Q4 2025 Earnings Call Transcript")

")

Introduction

For investors that are seeking a strong and stable divide income play I think that Everest Group Ltd (NYSE:EG) offers a lot of potential right now. The company has managed to grow the bottom line quite well over the years at 4.84% annually in the last decade. If this is something that can be sustained and also with a dividend yield of around 1.7% then EG looks like a stable addition to a portfolio as a backbone income play.

The company engages in the insurance and reinsurance industry which is heavily reliant on proper risk management and mitigating losses as much as possible is a key priority. I think that the margins for EG look solid as the company has managed to achieve an ROE of 12.1% and an ROA of 7.3%. These are strong margins and further underscore the efficiency of the business. Trading at a near 10% discount rate based on earnings to the sector is amplifying the buy thesis further.

Company Structure

EG stands as the seventh-largest reinsurance company globally, steadily expanding its presence in specialty insurance offerings. These encompass a diverse range of products, from Workers’ Comp insurance to short-tail property insurance and accident and health insurance, among others. EG strategically divides its business into two core aspects: reinsurance, which covers financial lines, casualty, and property, contributing $9.3 billion in sales in 2022. Since then it has continued to grow very well and EG still exhibits a lot of growth potential I think.

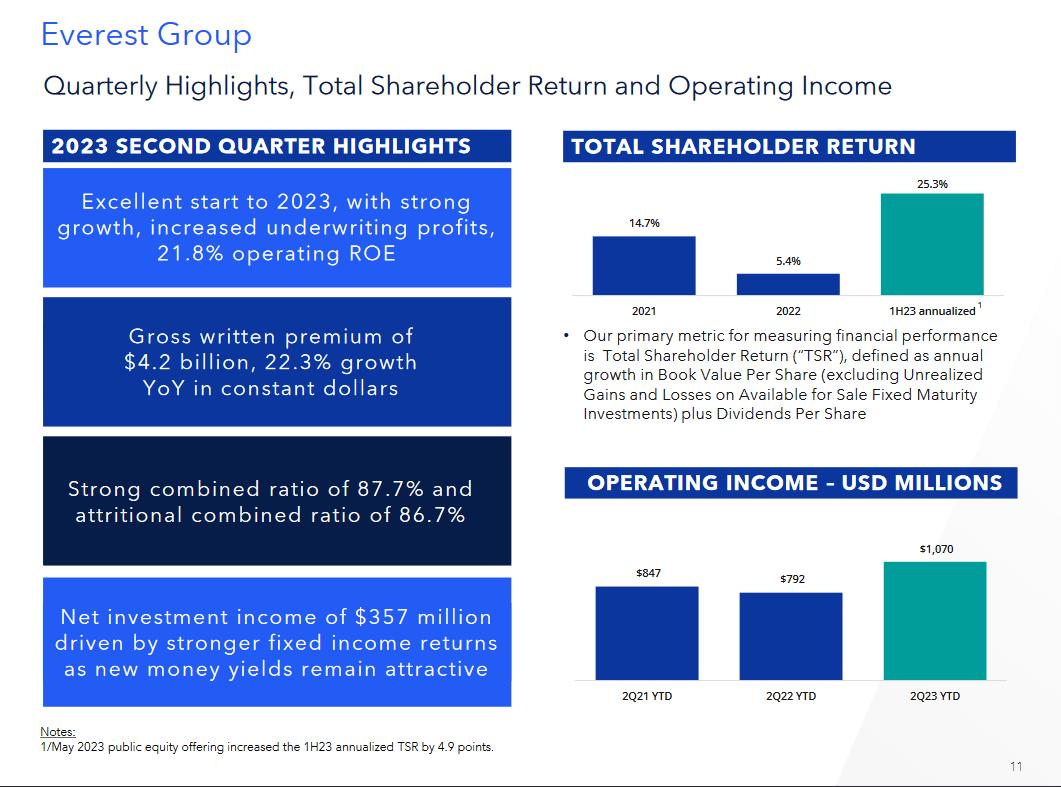

Company Overview (Investor Presentation)

Looking at the latest report from the company I think it has become clear that EG can perform very well in most market conditions. The current environment is difficult to navigate with possible declining demand because of higher interest rates, but the gross premiums written have climbed an astounding 22.3% YoY for EG. With the investments the company is making the bottom line has further improved as well. The net investment income was $357 million for the last quarter alone which was heavily driven by stronger fixed income returns for the company.

p/e (Seeking Alpha)

As for the valuation of the company, I think it remains very attractive still. The p/e sits below the rest of the select at just over 8. This is nearly 20% below the historical valuation of the business. I think that a large part of this decline has been the increase in interest rates that have made investors slightly worried and ultimately resulted in the decline in p/e. But for us investors, this just leaves a better buying opportunity I think.

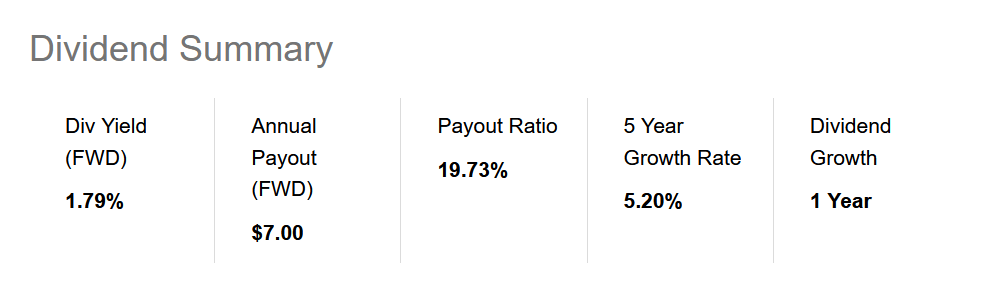

Dividend Summary (Seeking Alpha)

Adding to the buy case I think is the fact that EG has been raising the dividend recently quite well as a result of stronger earnings potential. The payout ratio I think is quite low as well and could go up to 30 – 40% without overleveraging the company too much right now.

Earnings Transcript

In late July EG held its last earnings call and as we know the quarter showcased a lot of strength so getting some more insight on the performance from the management team was well-needed I think. The CEO of EG Juan Andrade had the following to share with investors.

-

“We have strong momentum across the board. Capitalizing on the hard market opportunity in reinsurance, which continues globally, and both underwriting businesses continue to benefit from the global flight to quality amidst excellent and persistent market conditions”.

The higher interest rates may have some impacts on the company’s performance but I think that it has been shown that the market presence and positioning of the business have been in their favor and I would expect them to continue deriving a lot of value from this in the reinsurance space.

-

“International growth was strong, particularly in Asia, where we nimbly took share in dislocated markets like South Korea. Pretax catastrophe losses were modest despite the active cap order for the industry. Our deliberate initiatives to shape the portfolio and manage volatility continue to improve our results”.

Given the global presence, the company can reliably when necessary lean into more growing and promising markets around the world, one of them being Asia right now. I think that going forward seeing this type of momentum for EG is further adding support for a higher valuation. Being able to offset some challenges in other markets by focusing on growing ones should ultimately lead to more reliable and steadily growing earnings for the business.

Risk Associated

EG continues to navigate a landscape of growing regulatory and financial intricacies, particularly due to its segmented structure and geographic diversity. This complexity can pose challenges, potentially affecting EG’s operational flexibility. In the face of heightened stressors, the company may encounter hurdles in maintaining its long-term growth trajectory and cash flow generation potential. The last quarter showcased some strength though as the pricing conditions improved. I think this is the first thing that will deteriorate and post a warning sign that earnings for EG may fall.

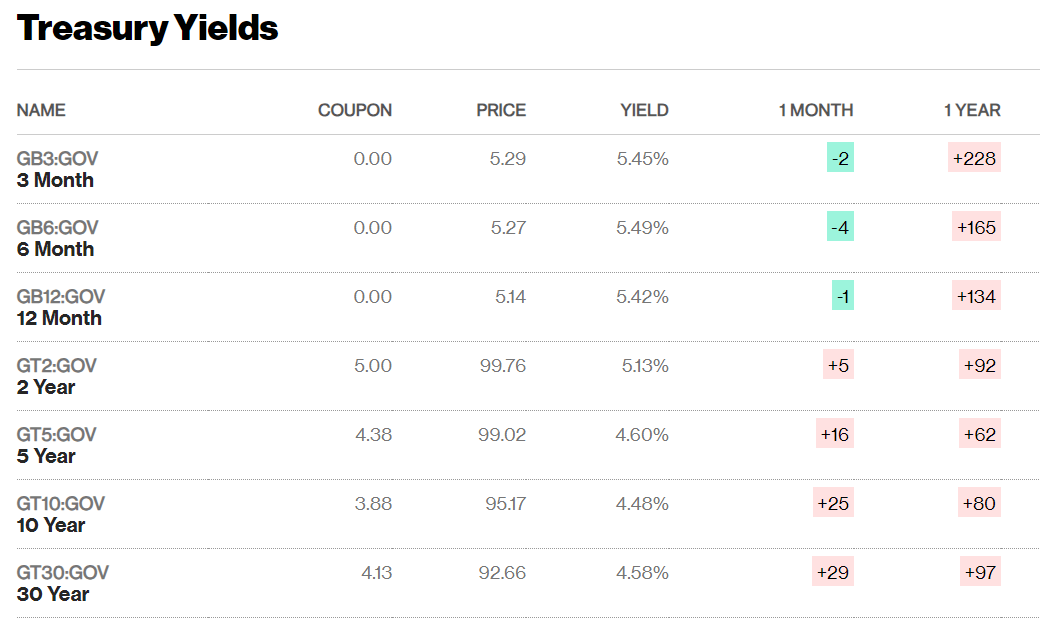

Treasury Yields (CNBC)

The insurance industry has faced challenges in outperforming the broader market due to its exposure to fixed-rate bonds, which exhibit an inverse relationship with interest rates. This dynamic impacts EG, especially in its reinsurance market, as rising interest rates can lead to reduced demand, affecting insurers’ net incomes and potentially hindering scale growth. If the fixed-rate bonds continue to largely underperform I think that the bottom line may be subject to a decline in the coming years. Furthermore, as the interest rates are climbing in the US the demand is likely to go down as well but this should be shortlived I think. My view on the interest rates is that they will remain elevated for the better part of 2024 and then begin to go down. Once they go down the bonds will likely appreciate and yield stronger earnings potential to companies like EG. Over time this should provide stable growth through the cycle and showcase why EG is a sound addition to a portfolio.

Investor Takeaway

EG has made a lot of progress over the years and right now is in a very favorable position I think to continue and grow very well over the coming several years. For investors that seek a broad and well-diversified insurance and reinsurance company EG looks solid. With a dividend as well that I think could showcase strong single-digit growth over the coming decade, it bolsters the buy case further. I am rating EG a buy now.

Read the full article here

Q4 2025 Earnings Call Transcript")

")

")

")

")

")

")

")