Q4 2025 Earnings Call Transcript")

")

")

Over the past three years, volatility has caused many investors to flock toward alternative “inflation hedge” assets. Gold performed very well during the initial government stimulus programs and QE efforts in 2020. Since then, it has not held its weight, primarily due to rising interest rates pushing the value of the US dollar higher. Admittedly, precious metals and miners have been one of my better market nuisances over this period. In early 2020, I was correct in being very bullish on precious metals due to expected inflation created by the Federal Reserve’s aggressive stimulus. However, I have generally maintained a bullish outlook since then, last detailing my bullish perspective on gold miners in May.

My perspective on precious metals has not proven correct since it was published. The critical difference between my precious metals outlook and the market’s reality is the surge in the US dollar’s value, combined with a continued sharp increase in real interest rates. In my view, it is correct to say that inflation has lasted longer than expected; however, it is a surprise that the Federal Reserve has maintained interest rate pressures despite the apparent declines in economic growth. Had the Federal Reserve backed off earlier this year when economic stability metrics waned, real rates would likely be lower, and gold and miners would be much stronger. That said, the Federal Reserve has maintained a very hawkish focus, primarily due to resilience in the job market.

Most gold miners, such as those in the VanEck Gold Miners ETF (NYSEARCA:GDX), are trading back near historical lows, erasing all gains since 2020 after losing a quarter of their value over the past six months. Notably, the price of gold has generally maintained a high level, still over a third above its pre-COVID range at ~$1815/oz. Thus, the weakness in gold miners may be attributable to either “P/E” valuation declines or a sharp increase in gold mining costs. Given this, I believe it is an excellent opportunity to take another look at gold and gold miners to assess the market’s rebound potential better or to revise my previous outlook.

Gold and Interest Rate Conundrums

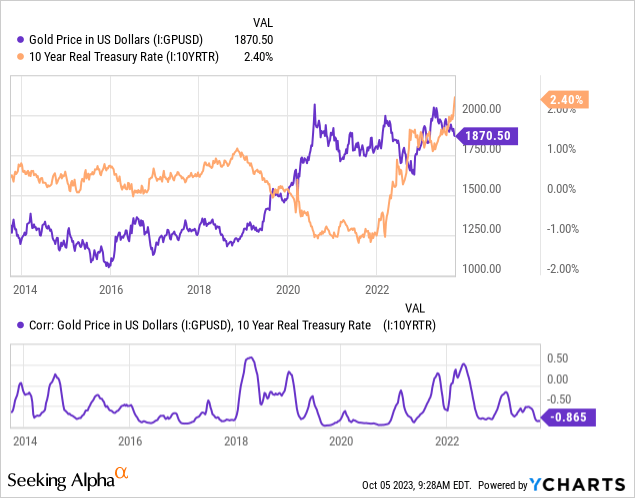

While gold is often viewed as a hedge against inflation, it is better understood as a hedge against interest rates and the inflation outlook. For example, in 2020, gold soared in value due to expected future inflation and a sharp decline in the carrying value of fiat currency (i.e., lower interest rates). Today, expected future inflation has moderated considerably while the carrying value of fiat currency is exceptionally high, making the money market a much higher-yielding investment than gold (after inflation).

Fundamentally, gold and inflation-linked Treasury bonds are “real assets,” but gold differs by paying no interest after inflation. Thus, gold is effectively discounted to the real interest rate. There is a robust inverse correlation between the real Treasury rate and the price of gold. See below:

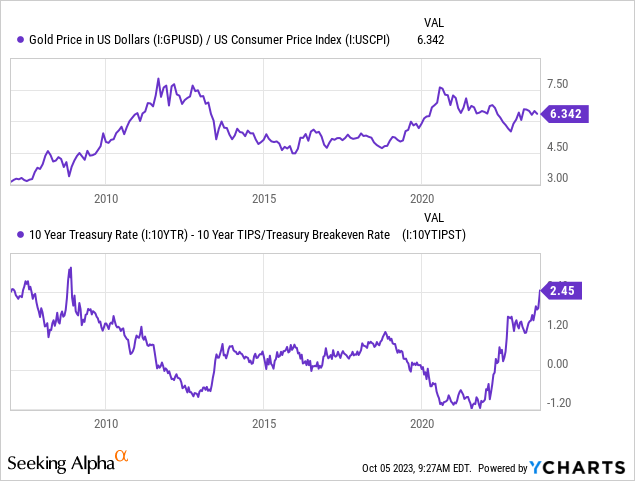

Of course, gold is also an inflation hedge, so it is most accurate to measure the real interest rate vs. the inflation-adjusted price of gold. Gold is still nearly as expensive today as it was in 2020, but its value in inflation-adjusted terms has declined a bit due to the rise in prices. Accounting for this makes the gold and real-rate relationship even stronger on a fundamental basis. See below:

Note the “inflation-adjusted” gold price unit is arbitrary since it uses the CPI. For example, today’s price of gold is 6.34 X the CPI (currently ~306).

Using these data, I calculated a relatively consistent inverse correlation of -0.8 between the two metrics over the past fifteen years. The slope on linear regression is ~-0.93, with a 6.07 intercept. Again, these numbers have little meaning since the units are arbitrary, but they can be used to calculate the price of gold based on real interest rates and the CPI today. With a 2.45% real yield, an extremely high figure, the “inflation-adjusted” fair value of gold, based on this simple model, is 3.8 times the CPI, or $1,163/oz.

Obviously, that is an extremely low price compared to the current price of gold. However, around 2006-2007, the 10-year real yield was around 2.45%, and the price of gold was ~$650/oz. In today’s dollars, that would be roughly $1,010/oz, indicating the same model would have overestimated the price of gold back then. Based on this model, we expect gold to rise and fall by nearly ~$300/oz for every 1% change in the 10-year real interest rate on US Treasury bonds. While this model is widely off today, it is relatively accurate historically, having an “r-squared” of around 63%.

Without a doubt, some variables could be added to the model that may make it more accurate and justify a higher price of gold today. Still, it is undoubtedly challenging to justify the current $1815/oz gold price in light of the extremely high returns after inflation on 10-year Treasury bonds. For one, gold may be overvalued due to excessive investor interest, rising from public concern over black swan events and governmental issues since 2020. This is reflected in the immense demand for physical bullion.

Secondly, the 10-year real interest rate may not be entirely accurate today if inflation is consistently understated by 2% to 4%, as some private models suggest, arguing that the CPI does not measure true inflation since it does not entirely account for out-of-pocket living expenses (and notably, insurance premiums). If inflation is 2% higher than suggested by the CPI, today’s “real interest rate” would be 0.45% (roughly its long-term average), modeling gold at ~5.65 times the CPI or ~$1730/oz, much closer to its current price. Of course, a slightly higher gold price would be justified if the CPI is lower than it should be.

This point is tied to the previous one because people may be particularly interested in gold bullion because they feel inflation will be higher than the CPI inflation outlook suggests. This is crucial for gold miners because gold could be significantly overvalued or undervalued based on how inflation is measured. There is also the incalculable risk that inflation surprises significantly to the upside over the coming years as the US government takes on its tremendous debt and interest rate load. This “upside tail risk” in inflation is a major bullish factor for gold that is not directly measured.

The US Dollar and Global Gold Mining Costs

Much of the gold produced by the companies in the GDX is international. Only 14% of the ETF’s assets are headquartered in the US, 43% are in Canada, and the rest are spread worldwide. Of course, many international miners are headquartered in Canada for regulatory reasons but mine in Africa, South America, and Asia. Notably, many large and small gold miners, some of whom are in GDX, have faced issues relating to human rights and environmental problems in those areas (mainly Africa), exposing GDX to the ongoing political issues in Africa. As some African countries look to reduce Western exposure and nationalize or regulate mining, I suspect many miners in GDX will face higher production costs and taxes.

Gold mining all-in-sustaining costs have risen dramatically over recent years, from around $960/oz in Q3 of 2020 to roughly $1350/oz by Q1 of this year. That represents a ~14.5% annualized cost increase, well above the inflation rate indicated by CPI. Since early 2020, there has been no overall change in the profitability of gold mining since the price and costs have risen to roughly the same extent. GDX is also trading at about the same price it was in early 2020, indicating the valuations and profitability of top miners today are unchanged over the past 3-4 years.

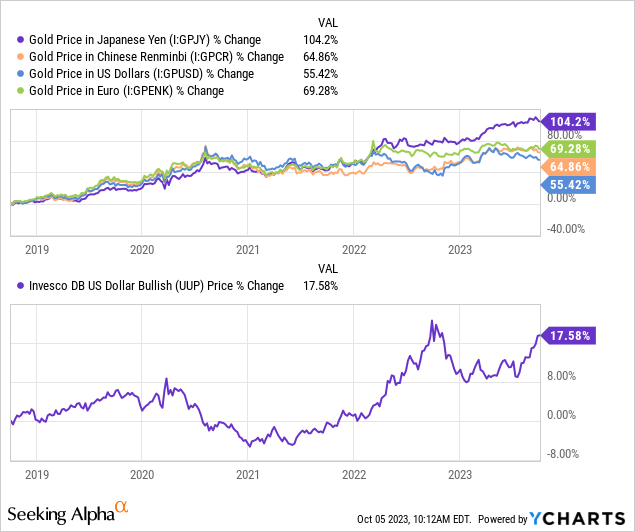

Political and economic issues in African and South American countries may continue to create pressure on gold production costs. High wage inflation and increased energy prices in developed nations also contribute to higher gold mining costs. Of course, while a strong US dollar lowers the US gold price, it is generally beneficial for GDX because its COGS decline in US dollar terms with a more substantial exchange rate. Today, gold is at an all-time high in Japan and China and is the weakest in the US due to the strong dollar. See below:

A strong dollar is bearish for gold prices but is more neutral for GDX because its constituents produce gold globally. Still, action in the US dollar will be necessary over the coming months. In the past, I believed the dollar would likely decline from its high value as Japan increased interest rates in line with its international peers. Despite Japan’s high inflation, its central bank has maintained negative interest rates. Japan has had to utilize direct FX market intervention to combat the currency collapse associated with this.

My long-term view has been that the US will end up similar to Japan, with the central bank becoming dovish despite inflation due to economic concerns. If you are in Japan, gold and gold miners would likely be an excellent investment today; however, thus far, the Federal Reserve and ECB have maintained a hawkish pattern despite weakening economic prospects. If this pattern continues in the US, the US dollar could break out above its past high, likely sending gold lower and reigniting currency instability in many countries. Of course, with the US dollar retesting its 2022 peak, a bearish correction would also be reasonable, potentially benefiting the price of gold, though likely having less of an impact on GDX.

The Bottom Line

Overall, I have a neutral outlook on GDX today and do not expect it to be particularly volatile over the coming months. My previous bullish outlook was based on the possibility of the Federal Reserve making a dovish pivot due to slowing manufacturing growth and weakening consumer spending. Initial jobless claims have been low after rising earlier this year, suggesting that the Federal Reserve can maintain a hawkish stance for some time.

In my view, crude oil will likely be a key deciding factor, as a rise in oil prices would lift inflation and lower economic growth, likely resulting in lower real interest rates and a higher gold price. If we see oil continue to break out, gold may be a valuable asset ahead of a dovish pivot. That said, gold miners may still be best avoided due to the sharp increase in production costs and political issues in many gold-producing emerging markets.

GDX is likely trading at its fair value today, given its valuation is about the same as from 2016 to the beginning of 2020. While gold is around $300-$400/oz more expensive than in most of that period, gold production costs are roughly equally higher, so profit margins are now approximately the same. Gold itself may be overvalued based on real interest rates, but that depends significantly on inflation expectations and how inflation is measured. At this point, I do not believe there are significant immediate positive catalysts for gold that would support an increase in GDX’s constituent’s EPS. In the long term, I suspect we will see a gold breakout, but before then, the jobs market will likely need to sour, which could support a higher gold price if inflation remains high in a weakening economy. Thus, investors are probably best off waiting for gold’s fundamentals to improve before dipping back into GDX or other precious metal miners.

Read the full article here

Q4 2025 Earnings Call Transcript")

")

")

")

")

")

")

")