Q4 2025 Earnings Call Transcript")

")

")

(NYSE:IRM)")

Graham’s wisdom applied to IRM

Let me start with an overarching view first before diving into the details of Iron Mountain Incorporated (NYSE:IRM). Under the current macroeconomic environment, I believe downside protection via defensive stocks is far more important than pursuing growth. Against this broader view, the thesis of this article is to argue IRM is NOT a good choice as a defensive stock under current conditions. I will make my argument following the timeless wisdom of Ben Graham.

First, Graham firmly believed that stock valuation should be anchored by interest rates, and he developed several methods for investors to assess stock valuation based on interest rates. As an example, the following is a method quoted from his book The Intelligent Investor:

Our basic recommendation is that the stock portfolio, when acquired, should have an overall earnings/price ratio-the reverse of the P/E ratio-at least as high as the current high-grade bond rate. This would mean a P/E ratio no higher than 13.3 against an AA bond yield of 7.5%.

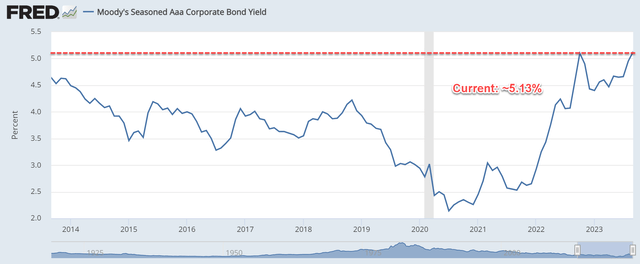

As you can see from the chart below, AAA bond rates (based on Moody’s Seasoned AAA bonds) are near the highest level in at least a decade, hovering around 5.13%. According to Graham’s wisdom above, this would mean a P/E ratio no higher than 19.5x.

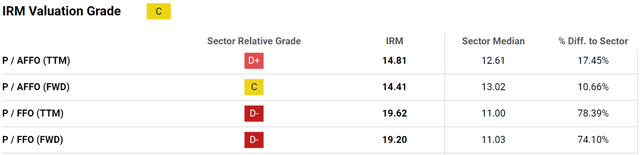

Now back to IRM, its P/FFO (the equivalent of P/E for REIT stocks) is in a range of 19.2 to 19.6x depending on if you use the TTM or FWD basis. Either way, its P/FFO ratio is too close to Graham’s guidelines and offers little margin of safety.

Some of you may argue that in terms of P/AFFO multiple, the stock is trading well below Graham’s guideline of 19.5x. It is true that its P/AFFO now sits in a range of 14.4 to 14.8x as shown in the second chart below.

To address this comment, my counterarguments are mainly twofold. First, many of the adjustments in AFFO feel quite subjective to me and could distort its true economic earnings. Second and more important, IRM’s credit rating is nowhere near AAA (its credit ratings are in the BB- to Ba3 range). And as a result, it shouldn’t be benchmarked against the AAA bonds rate to start with. Actually, as detailed in the section immediately below, its financial strength is another area that I am concerned with.

FRED Seeking Alpha

Graham on defensive stocks

Of course, it is important to note that the above valuation rule (or really, any valuation rule) should be just one of many factors that we consider when making investment decisions. Back to Graham’s wisdom, he also emphasized other factors such as the quality of the company’s earnings, financial strength, long-term growth record, etc. All these insights are distilled in his Intelligent Investor as a checklist for picking “defensive stocks.” At the top of his checklist is the following one:

Is the company large, prominent, and conservatively financed? The specific metrics to look for are stable financial strength, consistent capital structure, and a strong track record of dividend payouts.

Whether the company is a large and prominent player involves a bit of subjective judgment. On the one hand, it is a leading provider of records, documents, and information-management services. However, on the other hand, investors must be aware that this sub-sector is a relatively minor part of the economy in the grand scheme of things. At the same time, its traditional paper business is facing growth issues (paper records storage still is its core business currently) in our view. You can see more details on this in our earlier articles. Management has been trying to build out its information technology data centers. But this will require continued heavy investment (more on this in the risk section). In terms of dividend track record, the company has been paying and growing the dividend consecutively since 2010. A track record of 13 years is a bit too short for my liking. But it is a good start.

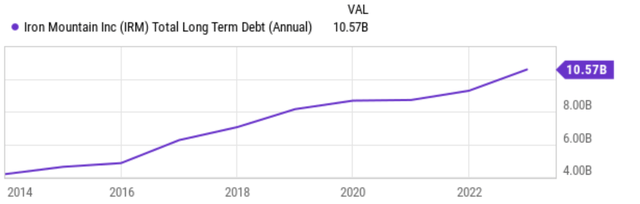

My bigger concern is with IRM’s current debt. And on this front, we do have more quantitative measures for more objective assessment. As seen in the top panel of the chart below, its debt has been rising rapidly. It has grown from about $4B to the current level of $10.6B in the past 10 years. Of course, this won’t be an issue if its earnings have also grown at the same pace.

Seeking Alpha

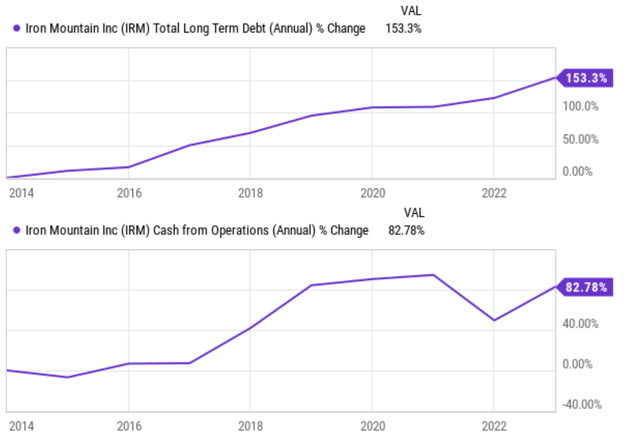

Unfortunately, this is not the case, as seen in the next chart below. The chart shows IRM’s debt growth (top panel) and earnings growth in terms of operation cash (bottom panel) in the past decade. As seen, IRM’s total long-term debt increased by 153.3% from 2014 to 2022. In comparison, its cash from operations increased only by 82.78% during this period. The debt growth has far outpaced its earnings growth.

Seeking Alpha

Other risks and final thoughts

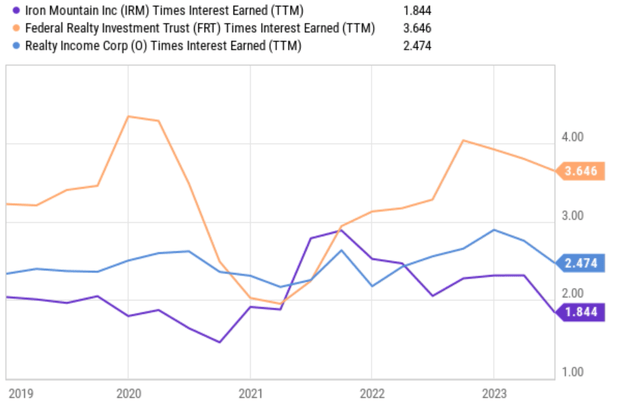

The financial stretch would cause other risks in the way I see things. As mentioned above, IRM’s debt growth has outpaced its earnings growth. To make things worse, the past few years have also witnessed a series of interest rate hikes, further adding to its borrowing cost. As a result, RM’s interest coverage, as shown in the chart below, is only about 1.84x now. It is near the lowest point in 5 years and also substantially below that of other real estate investment trust (“REIT”) stocks.

Such stretched financials can also limit its capital allocation choices. As aforementioned, management has been trying to build out its information technology data centers as a way to diversify its heavy reliance on paper records. On the positive side, I see this relatively new area as a promising growth engine for the future. At the same time, its core paper record segment is still generating healthy cash flow to bridge the transition/expansion.

However, this initiative into data centers will require continued CAPEX Investment for years. The stretched finances could limit management’s ability to pursue this expansion. In the meantime, time is not on IRM’s side, as competition is intensifying both from other entrants and also from more established cloud data center providers.

All told, I see the negatives as the stronger force under current conditions. To recap, my top concerns are twofold. First, its current valuation offers little margin of safety, especially when benchmarked against bond rates following the method Graham developed. Second, I don’t see it as a defensive stock given its stretched financial strength and the uncertainty of its growth initiatives.

Seeking Alpha

Read the full article here

Q4 2025 Earnings Call Transcript")

")

")

")

")

")

")

")