")

")

")

")

Walgreens Boots Alliance (NASDAQ:WBA) is one of the key players in the healthcare industry and one of the world’s largest retail pharmacies, headquartered in Deerfield, serving millions of people each year.

The company provides its customers with numerous services and products, including medicines, health and beauty products, and popular brands such as Soap & Glory, No7, Finest Nutrition, YourGoodSkin, and Sleek MakeUP. The company distributes its products through an extensive network of pharmacies, with approximately 13 thousand locations in Europe, the USA, and Latin America.

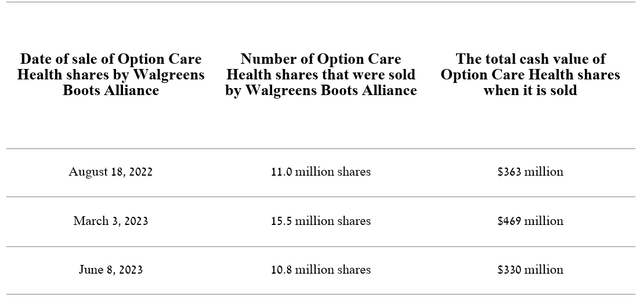

At the same time, due to Walgreens’ financial difficulties in recent years, its management continues to reduce its healthcare-focused investment portfolio. So, on December 15, 2022, Walgreens sold its stake in the Chinese company Guangzhou Pharmaceuticals for about $150 million. But more critical ones followed a little earlier. On August 18, 2022, Walgreens sold 11 million Option Care Health shares for $363 million. But management did not stop there and less than a year later sold the remaining stake in the company, one of the key providers of home infusion services in the United States.

Author’s elaboration, based on quarterly securities reports

While euphoria reigns in financial markets in recent months, caused by a sharp increase in investment interest in technology and commodity companies, Walgreens Boots Alliance continues to have a dark streak in its history.

We believe the major problems began after the company entered into agreements to pay billions of dollars to resolve thousands of lawsuits related to the opioid crisis. A few months after these events, Rosalind Brewer, who served as the Chief Executive Officer, and Hsiao Wang, the Chief Information Officer, left the company. Moreover, Walgreens Boots Alliance’s share price continued to decline after it was removed from the S&P 100 index in early September 2023.

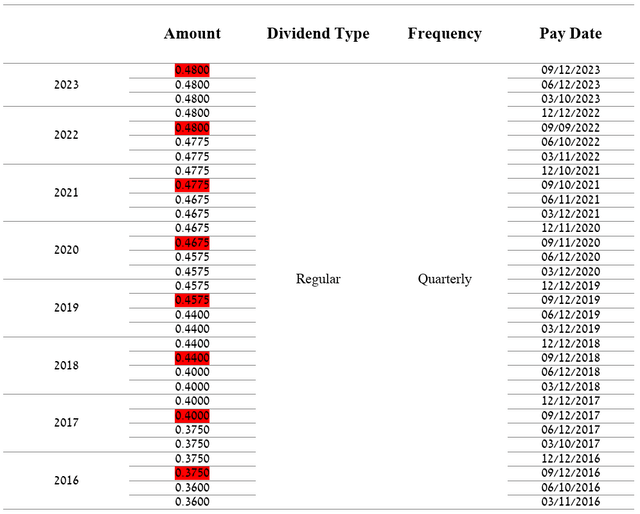

Additionally, we believe that Walgreens will have to reconsider its dividend policy, which has been in place for the past decades due to the sharp decline in its margins in the post-COVID-19 era, with the ultimate goal of keeping it from going bankrupt. One of the first steps in this direction was the announcement on July 12, 2023, that its board of directors left its quarterly dividend of 48 cents per share unchanged. This decision shocked financial market participants since the company usually announced an increase in dividend payments in July of previous years.

Author’s elaboration, based on Seeking Alpha

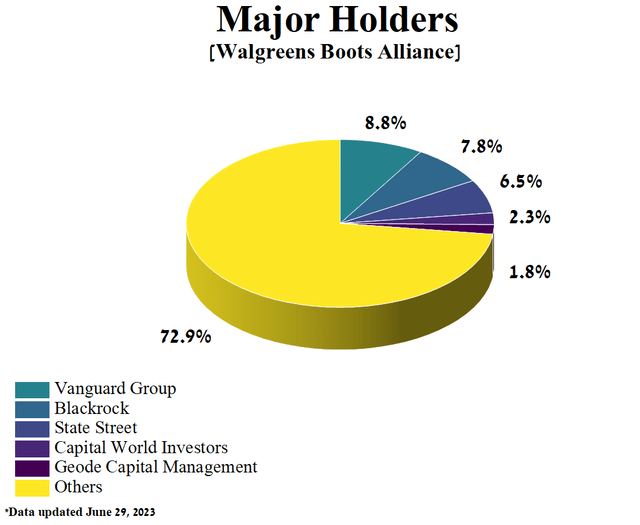

Nevertheless, despite a significant decline in the company’s gross margin in recent quarters and the suspension of dividend increases, Walgreens’ major shareholders, accounting for 27.09% of the company’s total stake, still include Wall Street giants such as Vanguard Group, State Street, Charles Schwab Investment Management, Geode Capital Management, and Blackrock.

Author’s elaboration, based on Yahoo Finance

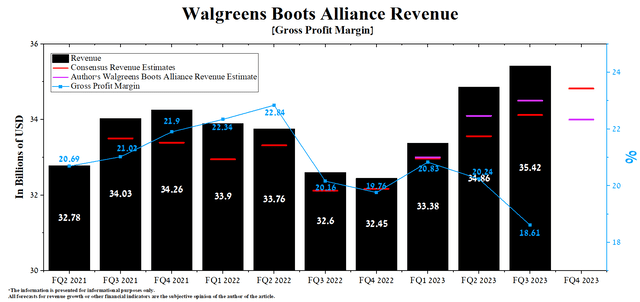

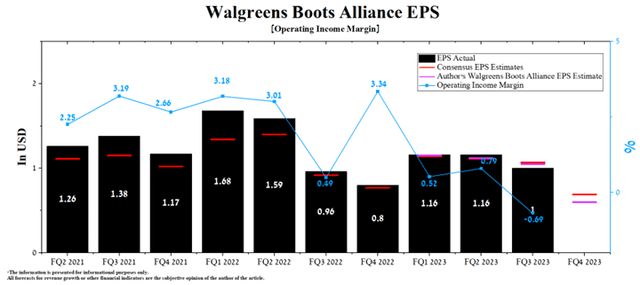

The third quarter of fiscal 2023 showed mixed results since, on the one hand, Walgreens Boots Alliance’s revenue was able to exceed analysts’ expectations, but on the other hand, it has been showing a decrease in EPS for several quarters. Moreover, the company’s management lowered its expectations for adjusted earnings per share for fiscal 2023 from $4.45-$4.65 to $4.00-$4.05 due in part to the continued slowdown in consumer spending growth in the United States.

On October 12, 2023, Walgreens will publish a report for the fourth quarter of fiscal 2023, which, in our opinion, will again upset investors. According to Seeking Alpha, the company’s revenue is expected to be $33.97-$35.76 billion, up 8.2% year-on-year and 2.1% higher than analysts’ expectations for the previous quarter. At the same time, our model projects Walgreens’ fourth-quarter fiscal 2023 revenue to fall at the lower boundary of this range, amounting to $34 billion.

Author’s elaboration, based on Seeking Alpha

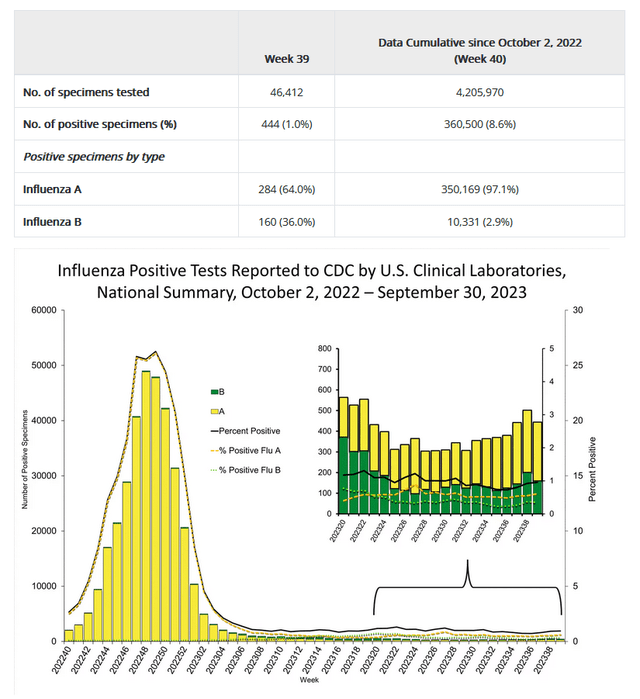

Walgreens Boots Alliance’s revenue decline relative to the previous quarter will be due to lower volumes of COVID-19 vaccinations and testing, a strengthening of the US dollar against other foreign currencies, and a weaker-than-expected number of flu cases in recent months.

Centers for Disease Control and Prevention

We forecast the company’s operating income margin to reach 0.1% for fiscal 2023. At the same time, for the 2024 financial year, this metric will drop to -0.2%. We expect this to happen due to a decline in consumer spending, which is also caused by the continuing trend of rising U.S. household debt. In addition, the continued increase in selling and administrative expenses due to the VillageMD clinic expansion will also negatively impact the company’s margins.

According to Seeking Alpha, Walgreens Boots Alliance’s EPS for the fourth quarter of fiscal 2023 is expected to be $0.66-$0.72, 35.5% lower than the consensus estimate for the third quarter of fiscal 2023. At the same time, according to our model, we are more pessimistic than Wall Street analysts and expect the company’s EPS to be $0.6.

Furthermore, the company’s Non-GAAP P/E [TTM] is 5.29x, 68.51% lower than the sector average and 40.44% lower than the average over the past five years. On the other hand, Walgreens’ Non-GAAP P/E [FWD] is 5.45x, which is one of the factors indicating its significant undervaluation by Mr. Market during a period of rising geopolitical tensions in the world.

Author’s elaboration, based on Seeking Alpha

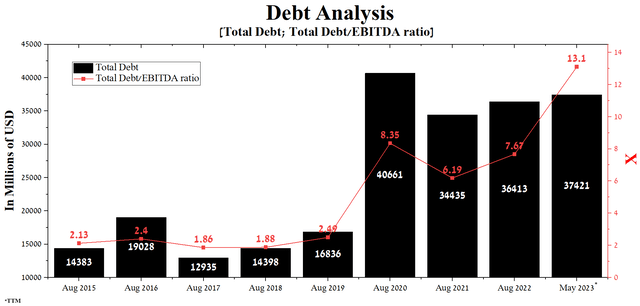

However, one of the key risks for the company remains its increase in debt from year to year, which also negatively affects its net income. At the end of the third quarter of fiscal 2023, Walgreens Boots Alliance’s total debt was about $37.4 billion, an increase of $2.99 billion over 2021. Moreover, due to the continued decline in EBITDA in recent quarters, the company’s total debt/EBITDA ratio increased from 6.19x to 13.1x.

Author’s elaboration, based on Seeking Alpha

Conclusion

Walgreens Boots Alliance is one of the key players in the healthcare industry and one of the world’s largest retail pharmacies, headquartered in Deerfield, serving millions of people each year.

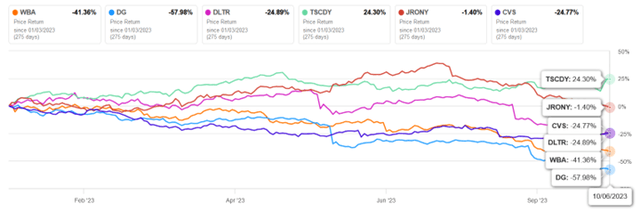

Despite the company’s revenue growth yearly, its operating income margin continues to decline. Additionally, the obligation to pay billions of dollars in settlements reached to resolve thousands of lawsuits related to the opioid crisis threatens Walgreens’s financial stability. As a result, the company’s share price has fallen more than 41% since the beginning of the year.

Author’s elaboration, based on Seeking Alpha

We expect the company to have difficulty repaying its USD, GBP, and EUR-denominated senior notes with a maturity date between 2024 and 2026. As a result, Walgreens Boots Alliance’s management will have to resort to painful steps, which may include mass layoffs and reductions in the number of its stores.

On the other hand, Walgreens’ extremely high dividend yield, which exceeds 8%, and our anticipation of the Fed’s interest rate cuts next year will contribute to maintaining optimism among some investors regarding the company’s future. Additionally, given the technical analysis, we believe that the price level at which the risk/reward profile would be attractive is $18-$18.5 per share.

We initiate our coverage of Walgreens Boots Alliance with a “hold” rating for the next 12 months.

Read the full article here

")

")

")

")

")

")

")

Q4 2025 Earnings Call Transcript")