")

")

")

Investment Thesis

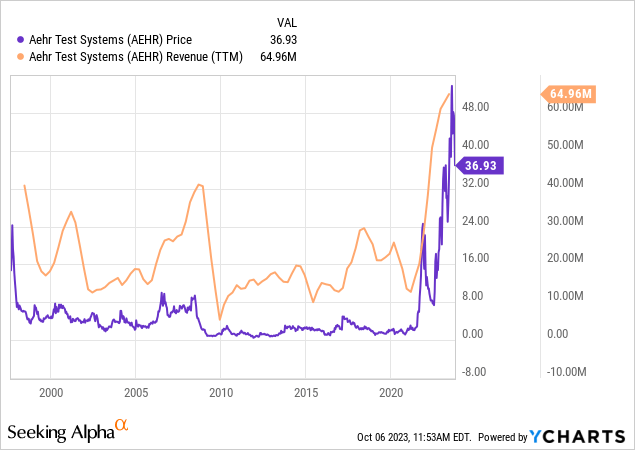

Aehr Test Systems (NASDAQ:AEHR) has been a hot topic recently, with its share price shooting up more than 2100% in the past two years. This big jump turned it from a penny stock to a company worth over $1.3 billion in 24 months.

The company sells testing systems that identify defects in semiconductor chips for production quality control. These devices are widely used by semiconductor companies, third-party labs, and OEMs. The test systems are designed to stress-test semiconductor devices in extreme conditions to ensure reliability and functionality.

The buzz around the company is all about growth. Aehr’s revenue jumped from around $15-$30 million to the $50-$65 million bracket and is expected to hit $100 million in sales this year. The figures are great, but do they justify the valuation? A deeper dive paints a more troubling picture that extends beyond the post-earnings 15% price decline after what the market saw as ‘disappointing’ Q1 2024 results.

Aehr’s Mixed Growth Narrative

A big chunk of Aehr’s growth comes from a contract it bagged from On Semiconductor (ON). It wasn’t because of some big market changes as much as a one-time opportunity which coincides with an accommodative market. As in any capital goods product, demand is cyclical.

Now, there’s talk about a broader trend from silicon carbide, a material used in the auto industry. The market for silicon carbide has been growing, but Aehr only recently started growing with it. So, although most of the shipped devices will be used to test silicon carbide wafers, one can’t really draw a linear relation.

This ties back to a bigger picture. Aehr came onto the scene way back in the 70s, but it hasn’t exactly grown in step with the semiconductor sector over the years. Its sales have had their ups and downs but never really hit a steady groove with the sector’s growth, even with all the big trends, way larger than the carbide scene. In other words, the current momentum is a rerun of an old show. And guess what? The boss who in my opinion didn’t quite steer the ship towards those growth waves back then is still at the helm, only now as the Chairman.

Another common argument often touted by Aehr is that Carbide chips have many defects, and that’s good for them because their devices test for these errors. But if you look back, you’ll see that making semiconductors has gotten better over time. So, even though carbide is the new kid on the block with a few hiccups, these kinks will likely get ironed out as things move along, which kind of pokes a hole in what Aehr’s bosses are saying in my view.

Product Portfolio

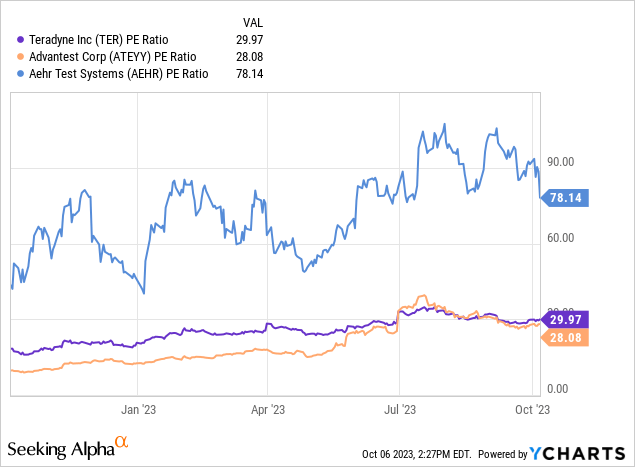

Management often says Aehr products are special. Features like exceptional parallelism, signal quality, and thermal accuracy are often cited. This might be true. Maybe not. But the fact is it’s a small player in a $5 billion Automated Testing Equipment ‘ATE’ market, which is mostly ruled by big names like Advantest (OTCPK:ATEYY) and Teradyne (TER).

Market positions of ATE players are hard to change and for a good reason. There are no uniform standards of testing. Every ATE company has its own ecosystem of programming language, software, user interface, and protocols. This, combined with a learning curve to operate and set up these devices, leads to consumer stickiness. This is likely why Aehr has remained a small player in the market and most likely will continue to be so. If its products are actually special [which I doubt], it is probably because it caters to a very specific audience.

When it comes to technology, Aehr hasn’t made a big splash. It’s been around since the 70s, doing pretty much the same thing, with no notable patents to its name. Out of the 37 patents in its name, 22 are expired, abandoned, or withdrawn. Many of the remaining 15 expire in the next few years. Its products have evolved a bit, adding the wafer-level testing in 2001, but the core technology hasn’t changed much. They don’t manufacture their products but assemble them in California.

Valuation

Aehr has historically grappled with sales concentration issues. While in recent quarters the performance has been satisfactory regarding revisions and meeting expectations, this hasn’t always been the case. Purchase delays are inevitable due to a myriad of reasons. Thus, the FY 2024 $100 million sales target is flexible.

That said, things look bullish on OnSemi’s side, with the company doubling down on expanding capacity to capitalize on favorable EV trends. OnSemi’s new facilities will be the home of some of Aehr’s FOX-XP, FOX-NP, Aligners, and Contractors.

Speaking of contractors, I find it odd that the company calls them consumables, which carry a connotation of recurring revenue in tandem with use. This is not entirely true. For years, Aehr’s customers for packaged RAMs (those using ATBS and MAX), which constitute most of its 2500 system installed base, have historically maintained product lines of the same chip designs, limiting the need for new contractors. Again, the relation between device and contractor sales are not linear.

As for valuation, a quick look at Seeking Alpha Quant Score rating shows that Aehr is overvalued compared to peers. The cyclicality and the $25-$30 million sales break-even point (Aehr historically needed to sell $25-$30 million worth of products to break even) add to the overvaluation narrative.

How I Could Be Wrong?

Since my last bit of caution on Aehr back in April, the price has actually hopped up by 27%. Clearly, my crystal ball isn’t flawless. The bullish ride might stretch longer than expected. More seriously, maybe there’s a genuine shift in Aehr’s market position. The semiconductor sector has a tight-lipped culture, and Aehr doesn’t spill much on how its customers are putting its gear to work to keep secrets of their manufacturing process and quality checks. So, the full picture will always be murky. And honestly, being a contrarian in this market isn’t easy with all the buzz going on. From tech upgrades to Biden’s Chip Act funneling chip makers closer to Aehr, there may be some good days ahead of them. What I’m trying to say here is that the current narrative doesn’t align with the company’s historical trends.

Summary

While the numbers look promising, Aehr’s growth seems more like a lucky break than a lasting success. As many microcaps are, the company is not in control of its destiny in my opinion. It might seem that Aehr is a mid-sized company, but with a $4.5 million quarterly net income, it’s more like a microcap with a midcap capitalization.

Management is selling shares, and none are buying on the open market. Geoff Scott, an independent director, cut his position from 114,668 shares to 34,990 shares this year. Aehr Chairman cut his position from 623,421 shares to 428,821 shares. Erikson Gayn, the company CEO, cut his holdings from 608,051 to 421,123 shares. Vernon Rogers’s shares declined nearly half, from 71,129 to 36,441. Alistair N Sporck, a Director, saw his shares decline from 14,062 to 12,651. These are notable declines, especially considering the figures above are net of stock-based compensation. For example, Gayn Erickson, Alistair Sporck, Adil Engineer, Don Richmond, and other directors received shares below market prices as part of their compensation, all at exactly $27.67 and $12.49 in October when Aehr’s share price was hovering in the $50s.

I believe that if management truly believes the company is on the edge of a fundamental breakthrough in market position, we wouldn’t be seeing a sell trend. My advice is to be careful and manage your risk. Since its foundation in the 1970s and IPO in the 1990s, Aehr never paid dividends. I don’t expect it to start soon. It’s a recurring narrative, a rerun of an old show – success always seems to be just around the corner. While Aehr occasionally exhibits growth, it largely mirrors the cyclical ups and downs of the industry in which it operates.

Read the full article here

")

")

")

")

")

")

")

Q4 2025 Earnings Call Transcript")