")

")

")

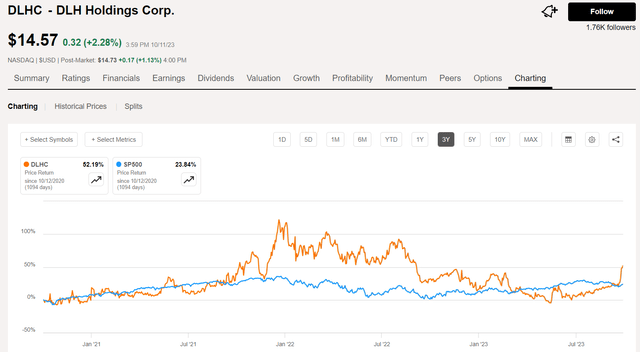

When I first wrote about DLH Holdings Corp (NASDAQ:DLHC) it was Veterans Day, 11/11/21. It seemed appropriate at the time to write about an underfollowed public company that specialized in the health and well-being of Federal employees, and one that had seen immense benefits from the Covid-19 pandemic. Multiple contracts were being awarded by the VA, FEMA, CDC, and other federal agencies to DLH for contract support services. At the time, the company had a market cap of about $250M with 2,200 employees and had just completed several acquisitions to further grow the business.

Back then I rated the stock a Strong Buy at a price of about $16 and it went higher until it reached about $20 in January 2022. Then in July 2022, I wrote a follow-up article suggesting that the stock was still a buy despite the short-term Covid contracts coming to an end. In fact, this was my conclusion at that time:

In my opinion, DLHC is a Strong Buy at current prices below $16 and represents an excellent opportunity for growth-oriented investors to buy into a small but growing and financially strong company that has excellent long-term potential.

Seeking Alpha

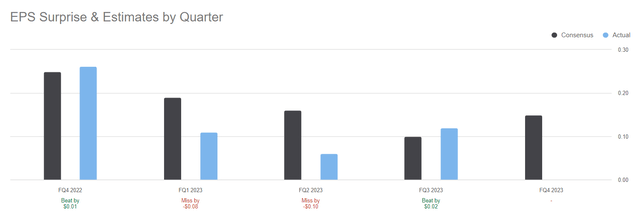

Unfortunately, things do not go as I had expected for the second half of 2022 and the first half of 2023 as revenues and earnings declined over that period, specifically in Q1 and Q2 of 2023 as can be seen in the earnings history chart from SA.

Seeking Alpha

Small cap stocks tend to be more volatile and even just one quarterly earnings miss can cause the stock price to be punished, which is what happened in the case of DLHC. But things are starting to look up again and earnings are again on the rise, with another acquisition completed since I last covered the name. With the recent improvements including beating earnings estimates in Q3 and rising forward EPS estimates, I think it is time to take a fresh look at DLHC stock and consider whether it is worth buying again.

DLHC Review

From the company’s website:

DLH delivers improved health and national security readiness solutions for federal programs through science research and development, systems engineering and integration, and digital transformation.

After the recent DLH Strengthens Information Technology and Cyber Capabilities through Acquisition of GRSi in December 2022 for $185M, the company now employs more than 3,200. According to CEO Zachary Parker, the GRSi deal marks the beginning of a new era for DLHC:

“Through this landmark transaction, we elevate our information technology and engineering capabilities, while adding the scale we need to thrive in an increasingly competitive marketplace. GRSi’s high-end IT and technical capabilities serving scientists, researchers, and system engineers have earned the company a reputation for excellence, and we expect that our unified organization will build upon those achievements to drive accelerated growth for DLH in the near- and long-terms. GRSi’s highly credentialed workforce features some the best and brightest technology leaders in our industry.”

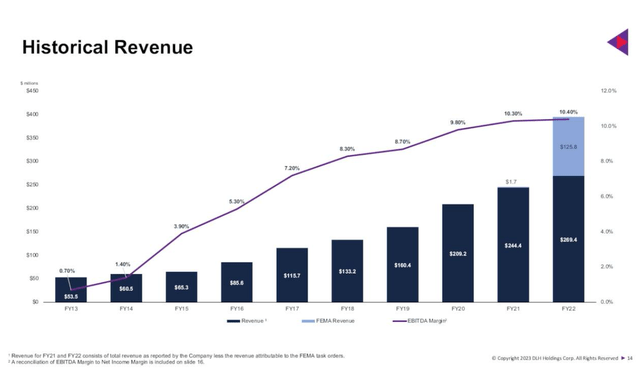

As of June 30, 2023, the company reported $102.2M in revenues for Q3 (the highest reported quarterly revenues in company history) with $11.3M in EBITDA and $7.1M in Operating Income with $0.12 diluted EPS. The reported backlog as of June 30 was $817.8M. From the Q3 presentation, the growth in annual revenue through FY22 can be seen along with the improving EBITDA margin over the company’s history. The FEMA revenues in FY22 were recognized from the DLH Wins FEMA Contract for COVID-19 Emergency Medical Services Throughout Alaska awarded for short-term emergency medical support for Alaska at the tail end of the Covid pandemic.

DLH Corp Q3 earnings

The company was recently awarded a new $85M 5-year IDIQ contract with the National Heart, Lung, and Blood Institute (NHLBI). According to CEO Parker, the company now has access to more value-added agency contracts than ever before with the ability to compete on many billion-dollar IDIQ contract vehicles in 2024. From the Q3 earnings call transcript, he had this to say about FY2024 potential:

Also, the White House fiscal 2024 preliminary budget called for historic investments in research, artificial intelligence and machine learning and digital transformation areas which would also boost our growth trajectory and bottom line performance. Our highly differentiated capabilities, broad area – a broad array of contracts and diversified suite of technology solutions make us a one-stop shop for advancing the government’s goals of tomorrow, and we look forward to what fiscal 2024 will bring.

Comparing YOY financials, it is apparent that Q3FY23 was a big improvement over Q3FY22. In particular, adjusted cash from operations improved 80% from $8.3M in FY22 to $15M in FY23. Also, a strong EBITDA improvement of $3M was offset by $2.4M in incremental non-cash depreciation and amortization related to the GRSi acquisition. Interest expense was higher by nearly $4.5M YOY but is being addressed by paying down floating rate debt and holding 60% fixed rate debt at 8%.

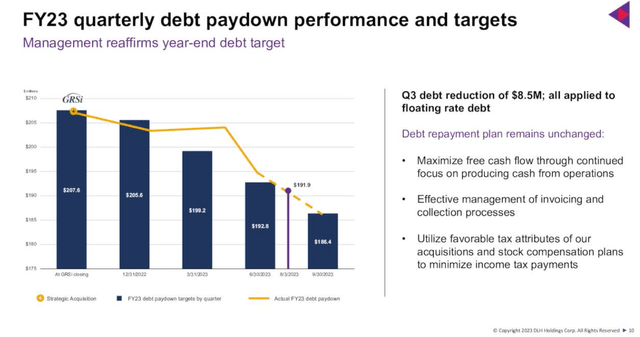

While the company’s debt load has been a concern, the company has been making strides towards paying down the debt and absorbing the GRSi assets. In Q3, $8.5M was applied toward debt reduction, with all of it paying down the floating rate portion of the debt as shown in this slide from the Q3 presentation.

DLH Corp

Valuation and Ratings

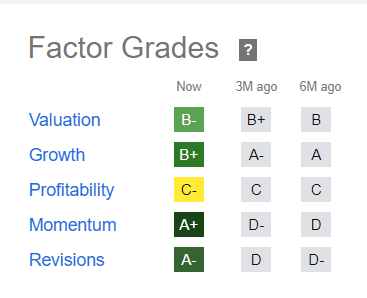

The stock is reasonably valued at the current price with a forward P/E of about 26x estimated EPS. However, the quant ratings show positive factors for Growth, Momentum, and Revisions with substantial improvement in Momentum and Revisions.

Seeking Alpha

Digging a little deeper into the Revisions, Earnings are expected to grow more than 90% in FY24.

Seeking Alpha

As we move forward in FY24, we should get more clarity in the revenue and earnings estimates as new contract awards are announced, assuming we do not experience another government shutdown in mid-November.

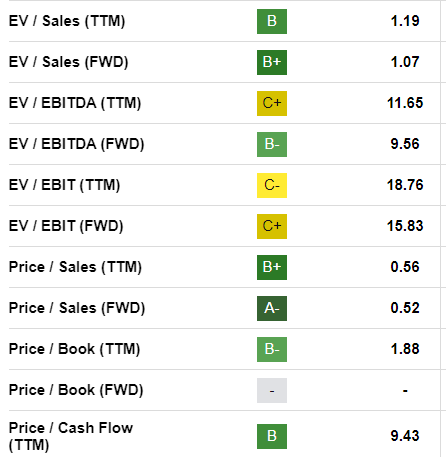

In addition, some of the other valuation metrics such as forward EV/Sales, forward Price/Sales, and Price/Cash Flow show promising future growth potential.

Seeking Alpha

The 1 Wall Street Analyst who follows the stock (Joe Gomes of Noble Financial), gives it a Strong Buy rating with a $21 price target. If the FY24 EPS estimate turns out to be accurate, that would result in a forward P/E of less than 14x, which is quite inexpensive for a growth stock. The $21 price target represents a forward P/E of about 20x the FY24 EPS estimate of $1.06. Over the past 3 years, the average P/E has been just under 20x so that seems quite achievable.

Seeking Alpha

Of course, all of the work that DLH performs is for federal government agencies which have been notoriously hamstrung this year by political infighting and budget constraints. Some of the already awarded IDIQ contracts have yet to see an RFP issued to perform any work under the contract. One question that was asked by analyst Joe Gomes on the earnings call was about that issue.

So I wanted to just start off, Zach, you mentioned about the IDIQs as you guys have won recently and it looks – in some of your prepared remarks in the earnings release, you talked about some of the difficult environment. Just trying to get a better idea of how you see some of those bigger IDIQs? When are they really going to start putting out opportunities for you to bid on new awards?

The response from CEO Zach Parker was cautiously optimistic but guarded (in my opinion):

We have been disappointed as you all know, with the government’s slowdown up until relatively recently as it relates to issuing new work on our previous IDIQs. I think I mentioned to you before, last time that our Defense Health Agency, Omnibus 4 IDIQ still has yet to issue the first request for a proposal. And we have been on standby with a real strong team for quite some time. That still continues to be the case, but we are starting to hear some – we’ve been very proactive on that, and we’re starting to hear that they are prepared, they’re getting closer and closer to prepared to issue a few of those. Similarly, we’ve had just slower than anticipated than government announced work on our – some of our other ones within NIH.

And then lastly, as you know, many of us across the industry, we’re anxiously looking for the government to resolve their process on the largest would be IDIQs, the CIO-SP4, it is where the biomedical research technology work is for largely health and human services agency is to be conducted, one that has been very strategic for DLH. We’re fortunate that in the heritage contract, the – our GRSi has some presence and some opportunities to pursue, but those will expand once CIO-SP4 before gets resolved.

Summary

While FY23 has been a somewhat challenging year for DLH, the company has made progress with the acquisition of GRSi gaining steam, debt levels are being reduced with operating cash flow, and the backlog of future work has increased although somewhat delayed in being awarded. As we approach the end of the fiscal year and FY24 begins, the opportunity for DLHC to see some accelerated growth looks encouraging, especially if the federal government can get its act together and start funding some of the work under existing IDIQ contracts that DLHC was previously awarded.

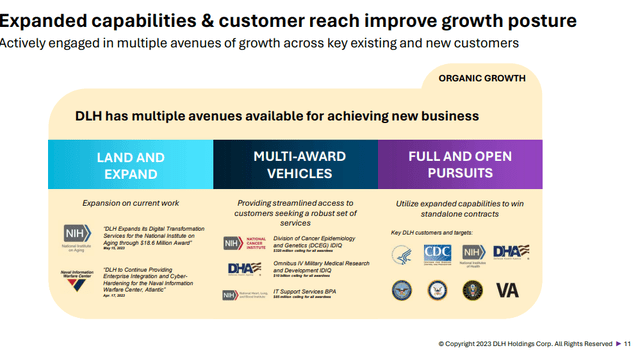

This slide from the Sidoti Micro-Cap Virtual conference presentation in August 2023 illustrates the many opportunities that await DLH between existing customers and new pursuits.

DLH Corp

I am still bullish on DLHC for long-term growth prospects and keep my Buy rating on the stock with the expectation that some good news is coming and will likely be announced when they report Q4 earnings next month. Unless the federal government gets into another budget impasse in mid-November, I believe that several agencies that have been delaying funding some of the previously awarded contracts will likely release those funds in the coming months and new contract awards will be announced.

Government agencies have a spend it or lose it mentality when it comes to budgets, and as long as the budgets for the agencies such as VA, CDC, and NIH are not cut drastically in 2024, I believe that DLHC will reap the benefits from their multiple awards and existing customer relationships.

Read the full article here

")

")

")

")

")

")

Q4 2025 Earnings Call Transcript")

")