")

")

")

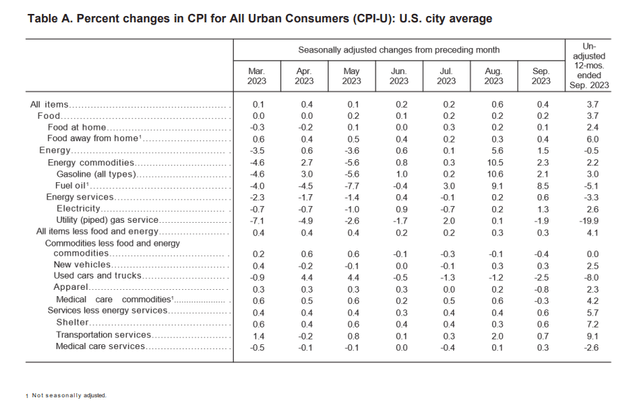

Stocks held steady in the face of a hotter-than-expected CPI report, although the headline rate held steady. Still, progress was shown on some critical elements known to matter to FOMC officials. Yesterday’s hot PPI print foreshadowed the unexpected strength today. Earlier in the day, the market sold off a bit, but as I predicted, there has been a significant pullback in the Volatility Index (VIX). The following details were in Thursday’s highly anticipated Consumer Price Index report:

BLS

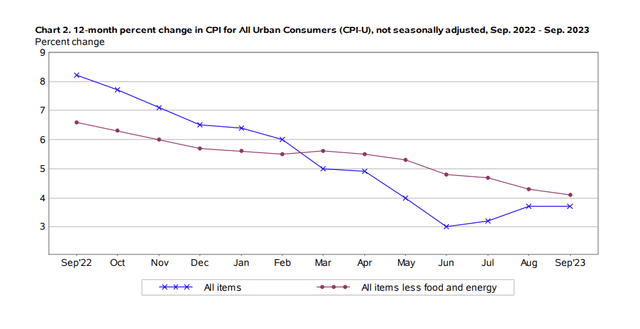

- Consumer prices rose 3.7% over last September.

- Prices increased at a monthly pace of 0.4%, higher than forecast by economists.

- The market initially sold off but then rallied. This is the market’s third time rallied on bad news in a week.

- Shelter comprised over 50% of the gains, and strong rents were part of the reason monthly gains were higher than expected.

- Current and leading housing indicators suggest weakness could be ahead in coming quarters, and much of the demand comes from wealthy borrowers less sensitive to rates.

- The price rise in gasoline was only 2.1% compared to 10.6% last month. However, the energy category was a net negative at -0.5%.

- Rates have risen quite a bit recently, and several Fed speakers have noted that this diminishes any urgency or requirement for the Fed to hike. This inflation report didn’t change that reality.

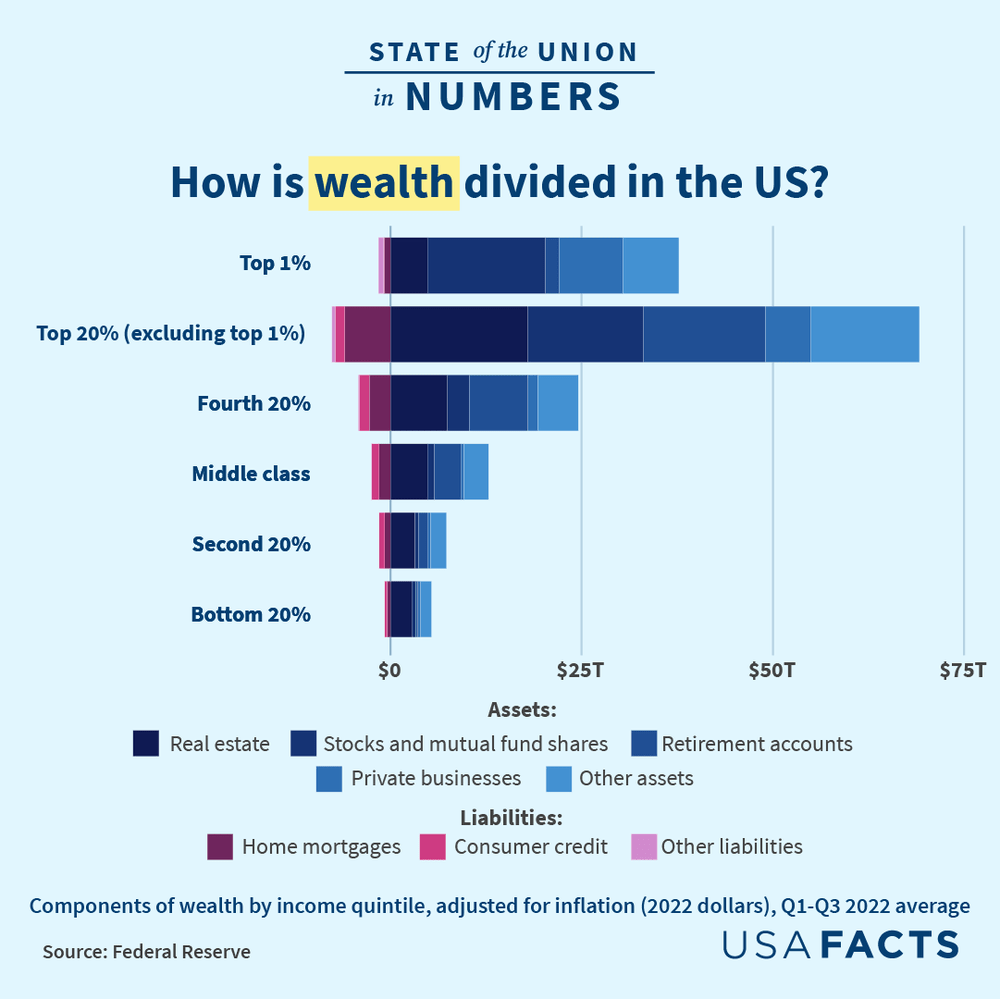

Overall, while the monthly increase was above expectations, there wasn’t a lot in this report to indicate the general trend in inflation has been uninterrupted. The other thing is this: Many categories are being driven by asymmetric per capita consumption by the wealthiest income quintile. One of the most significant economic changes since the last great struggle against inflation has been the extreme concentration of wealth to levels.

USAFacts.com

When I hear many bearish arguments about inflation, they seem to be grounded in the thinking of the 1980s Volcker-era economy in how they think about inflation. Well, it’s pretty apparent from many data sources that the economy has changed dramatically since then. One of the changes has been that the wealthiest in America have far more than they ever had in the second half of the 20th Century, and this changed consumption patterns. And where inflation is sticky due to these changes, primarily an extreme concentration of wealth.

BLS

You can see how this change is manifesting in the economy, and in some ways, it has likely made economic activity and employment more robust. For example, in the August CPI report, airline tickets and transportation costs were one of the most significant driving factors. A lot of the continued resilience in this category is because of the massive change our economy has experienced. The rich are so rich they can always afford to travel, buy homes, and eat out. Those areas are some of the stickiest areas of the CPI report, which shouldn’t be a coincidence.

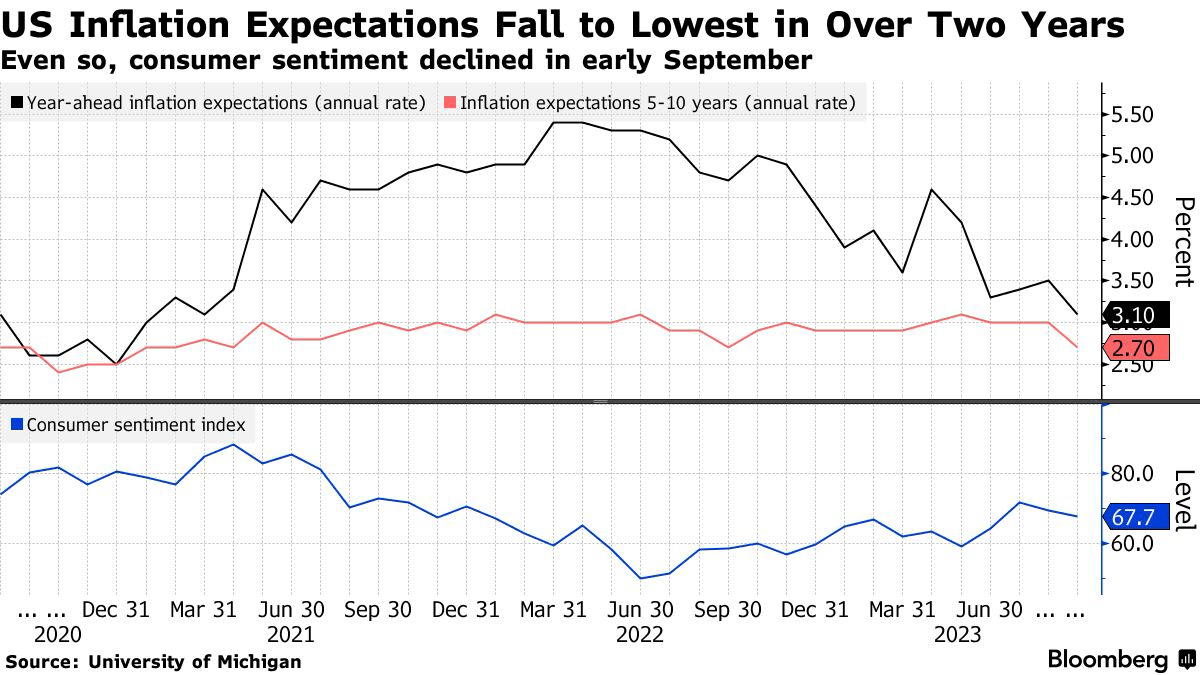

But the beneficial side of this coin is that it creates a robust labor market. And you can see this in the jobs report from this month. The solid numbers were driven mainly by new jobs in the food services industry. As the lower four quintiles of wealth run out of assistance, they return to the labor force. Since the rich are undeterred and have so much money, they never stop eating out, and the price increase won’t affect their behavior. However, I think this also explains some of the economic resilience in the data we are seeing. A lot of the stickier areas of inflation, like plane tickets and eating out, are areas the bottom four quintiles can avoid with pennywise behavior, which they seem to be doing. Generally, inflation expectations are where the Fed wants to see them as well.

Bloomberg

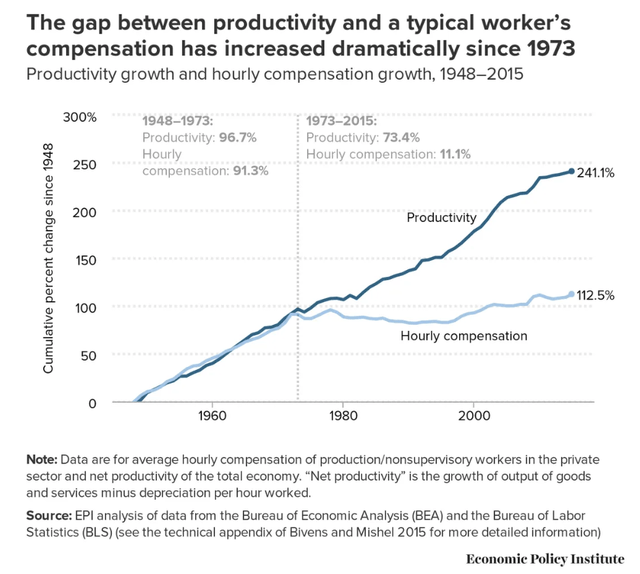

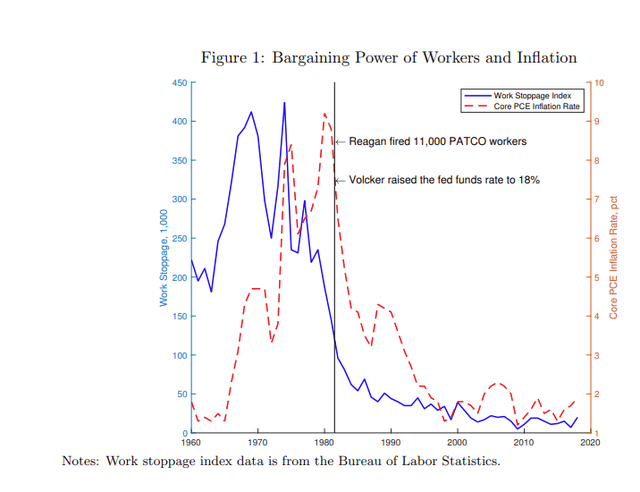

Of course, as investors, we must evaluate these matters dispassionately and based on the data to maximize our success. One of the best ways to achieve alpha is to understand the bounded rationality of your competition. I’ve noticed that Wall Street has certain cultural dispositions toward one of its favored thinkers, Milton Friedman. Of course, Mr. Friedman had some extreme views on how organized labor contributed to inflation. Still, since his theories were prevalent, organized labor has been gutted in the United States. The American worker is not able to exert upward pressure on wages they were in the 1970s and 1980s.

Economic Policy Institute

So, when you hear Bill Ackman say he’s shorting the 30-year Treasury because he thinks labor unions will keep inflation going long term, I would take that reason at least with a grain of salt. It would take labor unions probably at least a decade to return to having the impact on prices they have had in the past. The rise of tactics and tones from organized labor primarily comes from desperation, not a newly empowered state.

Federal Reserve

I’m a writer, and I know all too well that title selection factors significantly into how many people read your articles. Well, let me tell you something that sells on Wall Street: Doomsaying about labor unions that have already been defeated by management. I think judging the crowd and what the crowd thinks is essential. Using inaccurate beliefs of the crowd to boost your alpha is one of the quickest ways to outperformance, in my experience.

Also, I think the Fed knows that the rich are driving the stickiness of inflation and that an effort to mitigate their behavior through the wealth effect very well could destroy the village to save it.

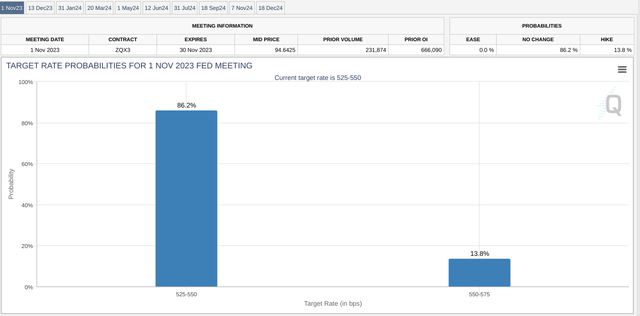

CME

I think the market’s reaction to this report broadly aligns with a conclusion I have advocated for some time now. In the wake of the CPI report, the odds of a Fed hike went down.

- Before Silicon Valley Bank’s collapse, I postulated that the Fed was calling the bond market’s bluff that it would “break something” and that they had a better grip on financial stability than consensus afforded.

- After the last Fed meeting, I stated that I believed the Fed would hike zero times or only one more time (one and done). That’s now the consensus view, but it was not then.

- I predicted there was potential for diminished volatility following the last jobs report after the sell-off caused by the ADP report. I got people into the Dow before its recent 13-day streak.

- Positive economic data are increasingly validating the possibility of a soft landing. Inflation is coming down convincingly and potentially persistently.

So, I’m pretty confident this report doesn’t change my central thesis on the Fed. Firstly, inflation has been largely defeated, and a “mop up” operation remains. Secondly, I think the Fed is done hiking and that recent upward pressure on rates has accomplished any tightening of financial conditions that would have been done with a further hike or two. Still, there are significant risks that could derail my thesis, to be sure.

Risks and Where I Could Be Wrong

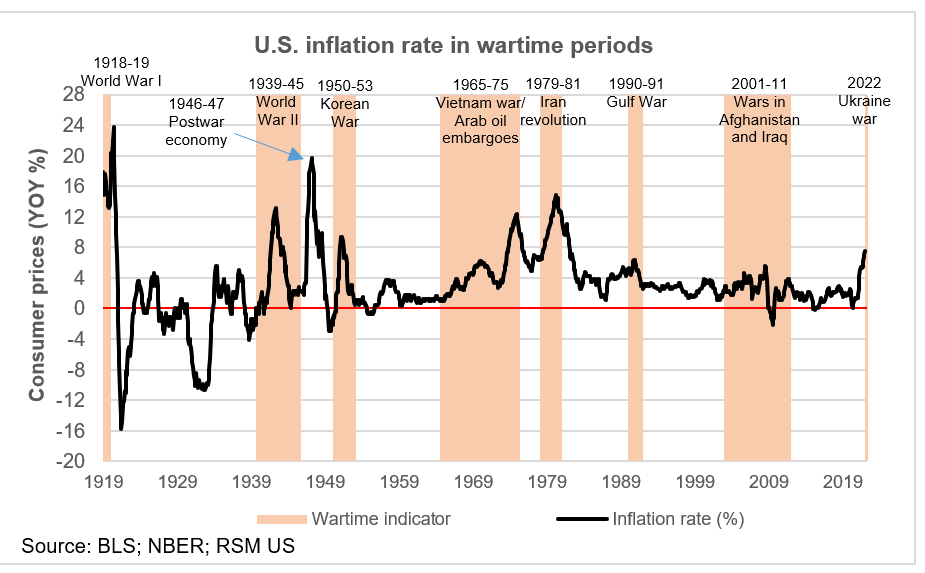

I’d say that the most significant risk by far for inflation is that we have deteriorating geopolitical conditions and rising conflict. Our last great about with inflation showed in stark relief how badly an expansion of the conflict in the Middle East could affect oil prices. For instance, if Iran and Israel become engaged in conflict, the region will likely become chaotic. Wars have historically driven inflation, and escalation of current conflicts or expansion of existing ones will likely cause the same.

The Real Economy Blog

There might even be significant physical obstacles to oil movement that could cause a shock. I do think this is a lower probability outcome, though. But it isn’t helped by a risky Biden Administration policy on the Strategic Petroleum Reserve. But we also must remember that the US place in global energy markets has changed a lot since our last about with inflation as well.

EIA

Wars have historically been a critical driver of inflation. Furthermore, as the winter dawns, Russia will likely begin attacking Ukraine’s energy infrastructure again. If there’s a frigid winter, energy prices could spike again. Recent agreements between Russia and Saudi Arabia aren’t encouraging in this vein. Furthermore, any of the following risks could exacerbate the chances inflation returns or that a more pernicious risk takes its place in the mind’s eye of the market.

- Escalation of geopolitical risks in China, Ukraine, or the Middle East.

- Fed policy error.

- Banking crisis worsens.

- Return of inflation.

- CRE meltdown.

- Write-downs of private assets.

Overall, I’m encouraged by the leading and current data showing progress on critical components of Shelter. I think this is one of the major things that gives the Fed comfort, and it also comforts me that my thesis is playing out correctly. I think the inflation battle has essentially been won, and the progression of the cycle and lag effects of monetary policy should hamper much of the remaining inflation. The wealthy may keep certain elements elevated, but not enough to justify fire and brimstone from the FOMC.

Conclusion

Saying that inflation is vanquished can be a tricky thing. However, when analyzing such an important economic issue as inflation, we must suspend our bias and understand how the economy changes. The reason that saying inflation is declining can be unpopular is that most Americans don’t feel this reality. They have seen prices rise, and their wages have not kept up with these rises, so from their perspective, it might be maddening to hear that inflation is declining.

Piketty/Saez/Zucman

However, I would argue that this is essentially a function of that exact economic change that keeps inflation sticky: The extreme concentration of wealth. Most gains, by far, from economic growth have gone to the wealthy, so the headline numbers look much better than the average person feels. However, financial conditions have tightened mainly on their own of term premium gains. I also find it unlikely that the Federal Reserve would bash the economy in such a fragile state, particularly given recent geopolitical developments, to incentivize the rich to stop buying plane tickets and vacation homes.

CNBC

The stock market has quite a herky-jerky reaction to today’s news, and rising rates spooked some optimistic gains that occurred earlier in the trading sessions. Still, I think this will ultimately be a buying opportunity until the end of the year. Performance has been lagging, and many fund managers will be incentivized to chase recent gains higher.

Read the full article here

")

")

")

")

")

")

Q4 2025 Earnings Call Transcript")

")