2026-04-29")

")

For over a year now, I have been familiarizing myself with many of the financial institutions out there. Most of my emphasis has been on small to medium sized banks. Few of them have had market capitalizations exceeding $10 billion. And many have been $2 billion in size or less. But one of the smallest has got to be Northeast Community Bancorp (NASDAQ:NECB), a firm with a market capitalization as of this writing of $188 million. But small does not necessarily mean bad. In fact, in this case, the small size of the bank probably works in the favor of investors. And that’s because the firm is currently flying under the radar of many analysts and investors alike. Digging deeper, shares look to be very attractive and the quality of assets appear high. Given these factors, combined with attractive growth that the bank has achieved in recent years, I have no choice but to rate it a ‘strong buy’.

A great little bank

According to the management team at Northeast Community Bancorp, the company is the owner of a New York state chartered savings bank that is headquartered in White Plains, New York. It was originally founded back in 1934 as a community-oriented firm. Over the years, it has grown to operate 11 branch offices located in several counties throughout New York, as well as three separate counties in Massachusetts. It also has three loan production offices, with two of those in New York and the other in Massachusetts.

Through this network, the bank engages in a wide variety of activities. For instance, it originates construction loans. That’s its primary emphasis. However, it does also issue loans that fall under the commercial and industrial category, the multifamily and mixed-use residential real estate category, and the non-residential real estate category. It provides customers with retail deposit services and, up until recently, it participated in the offering of investment advisory and financial planning services to certain clientele. However, in December of last year, the company agreed to sell off those particular operations in order to focus on its core activities.

Author – SEC EDGAR Data

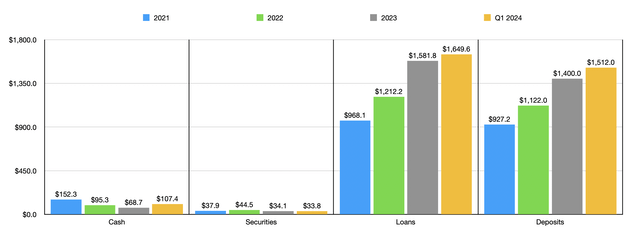

Over the past few years, management has done a great job of growing the institution. The value of deposits, for instance, jumped from $927.2 million in 2021 to $1.40 billion in 2023. This is an impressive growth rate amounting to 22.9% on an annualized basis. This growth continued through the first quarter of 2024, with deposits for that time totaling $1.51 billion. In addition to this, it’s worth noting that only 24.6% of its deposits are currently uninsured. When I look for financial institutions, I prefer this number to be as low as possible. However, I do have a threshold of 30% as being the maximum that I tend to accept. So to see this come under that number is great.

Over that same window of time, the value of loans on its books grew even more. They jumped from $968.1 million to $1.58 billion, before ultimately hitting $1.65 billion in the latest quarter. The largest chunk of these, about 78.2% in all, are construction loans. These are loans that are typically given out in $5 million or $10 million increments to customers. All combined though, they are on the balance sheet for $1.22 billion. Outside of this, the largest exposure would be residential real estate loans. That number comes out to $231.1 million, with $197.9 million of that amount being focused on multifamily properties. Commercial and industrial loans are in a distant third place at $108.9 million. The good news here is that there appears to be very little focused on long term office assets. This has been a weak spot in the loan and real estate market. It’s unclear what this number is. However, non-residential real estate loans totaled $19.1 million last year. It’s likely that this would include some office assets.

Author – SEC EDGAR Data

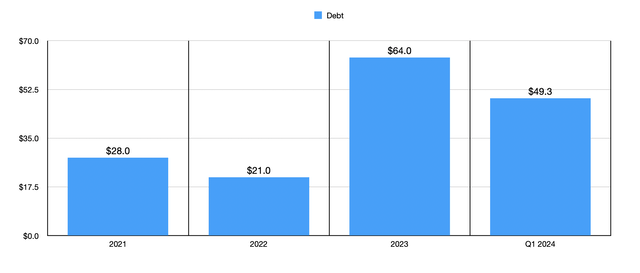

While deposits and loans went up, there was some weakness when it came to securities. However, the decline was only from $37.9 million to $34.1 million by 2023. As of the first quarter this year, securities fell further to $33.8 million. During the same three-year window of time, the value of cash and cash equivalents plummeted from $152.3 million to $68.7 million. Today, however, that number is back up to $107.4 million. Debt did roughly triple over this period to $64 million, but it has since fallen to $49.3 million as of the end of the first quarter for this year.

Author – SEC EDGAR Data

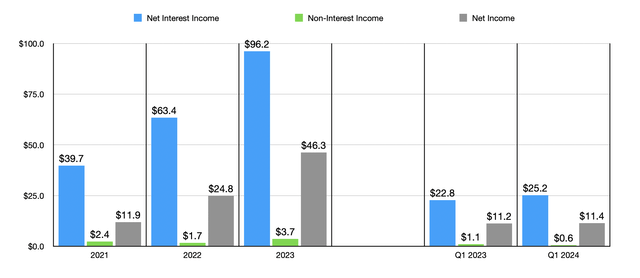

This overall growth of the institution has allowed revenue and profits to expand nicely. Net interest income went from $39.7 million in 2021 to $96.2 million in 2023. The growth in the company’s loan portfolio, combined with higher interest rates, was instrumental in pushing interest income from loans up significantly. In 2022, interest income was only $70 million. But last year, it was a whopping $127.5 million. Yes, higher interest rates and growth in debt caused some problems, such as an increase in interest expense from $8.1 million in 2022 to $35.3 million last year. But that didn’t stop net income from skyrocketing. Even though non-interest income budged only slightly from $2.4 million to $3.7 million, the growth achieved by net interest income helped net income to almost quadruple from $11.9 million to $46.3 million. For the first quarter, net interest income of $25.2 million did beat out the $22.8 million reported one year earlier, but the decline in non-interest from $1.1 million to $0.6 million caused net income to inch up only modestly from $11.2 million to $11.4 million.

Author – SEC EDGAR Data

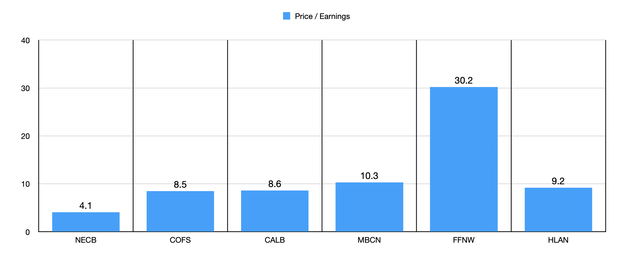

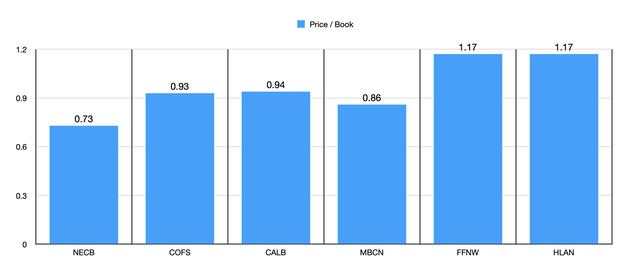

With these figures, it becomes pretty easy to value the company. In the chart above, you can see how shares are priced on a price to earnings basis. The stock is trading at a multiple of only 4.1. That’s one of the lowest that I have seen, and it’s perhaps the lowest I have seen in this space in months. That chart also shows, however, how shares are priced compared to similar banks. But of the six companies, Northeast Community Bancorp ended up being the cheapest. The same holds true when using the price to book multiple as shown in the chart below.

Author – SEC EDGAR Data

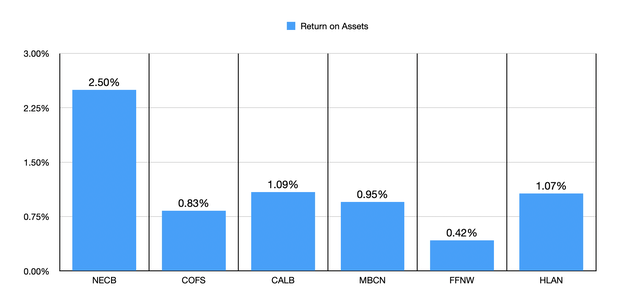

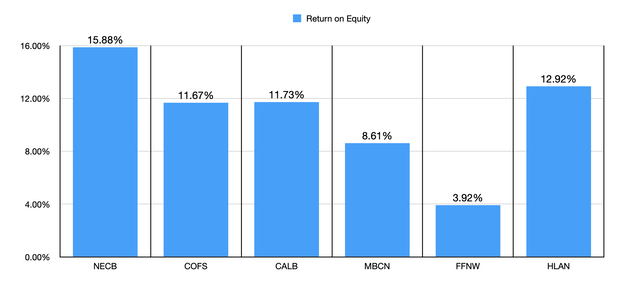

Attractiveness from a valuation perspective is important. But we should also be paying attention to asset quality. In the first chart below, you can see this process in action with the return on assets for the institution and the same five companies I’m comparing it to. With a reading of 2.50%, our prospect is the highest of the group. The same actually holds true when using the return on equity. This can be seen in the second chart below. With a reading of 15.88%, Northeast Community Bancorp is materially higher than the next highest of the five firms.

Author – SEC EDGAR Data

Author – SEC EDGAR Data

Takeaway

Based on the data provided, I must say that I am quite impressed by Northeast Community Bancorp. The bank seems to be doing really well. It has a solid track record of growth and shares are attractively priced on both an absolute basis and relative to similar enterprises. Asset quality has proven to be incredibly high. The firm has relatively little debt and strong profits. Add all of this together, and it’s difficult not to rate it a ‘strong buy’.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

2026-04-29")

")

")

")