2026-04-27")

")

Aptiv (NYSE:APTV) reported 1Q24 results that surpassed very low expectations, which helped to improve sentiment around the stock.

There were many things to like the report:

- 1Q24 revenues coming in-line while margins surpassed expectations.

- While guidance came down, they came down towards lower expectations, relieving investor fears that things are not as bad as it seems.

- The doubling of the share buyback target implies management sees Aptiv as undervalued and are confident in the future potential of the company.

- There were multiple commercial wins that were strategic and helped improve sentiment about Aptiv.

- Reducing of Motional equity stake and a corresponding EPS improvement as a result of it.

While this is the first article I publish about Aptiv on Seeking Alpha, I have written extensively about it in my Investing Group. I continue to be confident about the future prospects of Aptiv and see the current depressed sentiment as a good buying opportunity.

Let’s dive right into the 1Q24 quarter.

1Q24 review

Overall, I think that with the Aptiv 1Q24 quarter, given sentiment was already very poor, the somewhat in-line results had the effect of a beat.

While top-line was somewhat in-line with expectations, bottom-line managed to beat expectations despite depressed sentiment and a challenging environment.

Aptiv reported revenues of $4.9 billion, which was up 2% from the prior year. This was in-line with consensus.

Growth-over-Market (“GoM”) was 3%, compared to consensus expectation of 2%, with AS&UX GoM coming in at 6% and S&PS GoM coming in at 2%

Adjusted operating income came in at $544 million or 11.1% margin, beating consensus expectations of $487 million or 9.8% margin. The big surprise came from AS&UX margins coming in at 10.8%, 460 basis points ahead of consensus expectations.

This beat in AS&UX margins was due to multiple factors.

Firstly, the bulk of direct semiconductor inflation is now in the piece price.

Secondly, active safety is hitting volume levels where the flow through is better. This is important for Aptiv since active safety is the fastest growing product where growth has been about 20% this year and margins have been constrained. In addition, this does help alleviate concerns that this growth in active safety will be margin dilutive.

Lastly, the cost cutting actions that Aptiv has taken, which includes reducing overhead, moving engineering to lower cost countries have provided a leaner and more efficient cost structure going forward.

All in all, I think the AS&UX quarter shows us what can be for Aptiv. In the flat volumes’ kind of automotive environment, AS&UX was able to grow 6% over the market and achieve double-digit margins, which is really enviable. As such, it does give me confident in higher margins as growth returns.

Adjusted EPS was 1.16, beating consensus expectations by 15%.

Guidance

2024 revenue was guided down from the earlier range of $21.3 billion to $21.9 billion to the new lower range of $20.9 billion to $21.5 billion. This was largely due to lower production. Consensus expectations were at $21.5 billion, so the guidance revision downwards was actually within expectations, which probably helped alleviate some fears.

2024 operating income guidance was also revised down from the earlier range of $2.475 billion to $2.625 billion to the new range of $2.425 billion to $2.575 billion. That said, at the midpoint, the new range and earlier range had the same 11.8% operating margin. Consensus expectations for operating income were at $2.5 billion, so the new lower range was also in-line with expectations. The lower operating income guide was due to the lower sales but offset by cost and performance actions.

Management also raised the EPS guidance from $5.55 to $6.05 to the revised range of $5.80 to $6.30, due to the Motional deal and share repurchases.

Buybacks doubled

Aptiv repurchased stock worth $600 million in 1Q24.

In addition, management raised the full-year stock repurchase target to $1.5 billion.

As a result, in 2024, buyback is expected to double.

This was what management had to say about the doubling of the share repurchase target due to the undervaluation of the stock:

We continue to believe that our stock is undervalued and presents an attractive opportunity to return capital to shareholders. As such, we’re doubling our share repurchase target from $750 million to $1.5 billion during 2024

To me, this is a sign of confidence from management that they believe in their bookings and future growth potential and the margin improvement story,

In addition, it is also another sign from management that they believe the stock is undervalued.

The remaining $900 million in share repurchases for the rest of 2024 is approximately 4% of its market capitalization.

Looking forward, I think free cash flows will remain rather resilient, and I do not see it softening, but if anything, it should improve.

As a result of this aggressive stance on buybacks, it does signal to me that the company will continue to buy back stock if the stock remains depressed.

Commercial traction

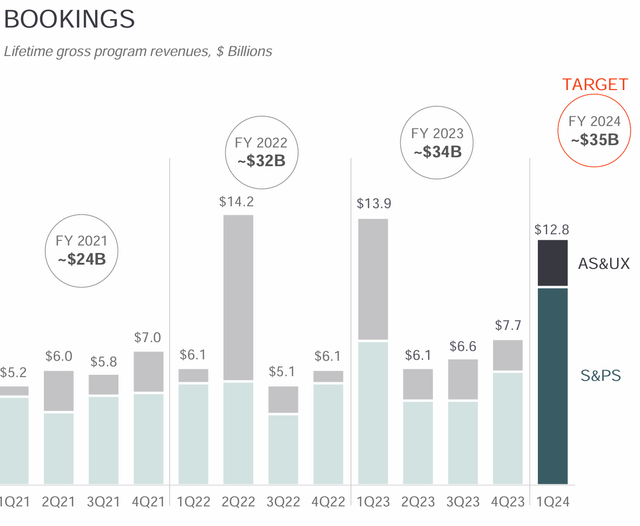

Bookings in 1Q24 quarter came in at $12.8 billion.

Given that Aptiv expects the total 2024 bookings to be $35 billion, it remains on track to achieve that. In 1Q24, AS&UX bookings came in at $2.5 billion while S&PS bookings came in at $10.3 billion.

Bookings (Aptiv)

The S&PS segment had a busy 1Q24 quarter with strong traction in multiple areas.

Firstly, there was strong traction with local Chinese OEMs in the quarter, with bookings of more than $1 billion across five local Chinese OEMs.

This is a huge deal for Aptiv given that it traditionally does not have exposure to the Chinese market through local Chinese OEMs, but rather through their joint ventures.

I think this does illustrate that Aptiv is starting to gain traction in China and bodes well for the long-term business potential for the company.

Secondly, there was a $1 billion architecture award with a major global OEM’s PHEV and BEV platforms in North America in 1Q24, along with another ICE platform win with an incumbent supplier.

All in all, this shows that Aptiv is winning across power trains.

Thirdly, Aptiv achieved its first power electronics win with a global EV OEM’s next-generation platform, and it also won a high voltage architecture award with a global truck manufacturer.

The AS&UX segment also saw significant wins.

Aptiv won additional radar awards with a Japanese OEM for both North America and Asia Pacific regions.

Also, Aptiv won a full system, productized ADAS award with an emerging EV partner. This emerging EV partner chose Aptiv’s Gen 6 ADAS platform, including its Wind River’s full stack for ADAS applications.

There was also a Studio Developer award for Wind River in 1Q24 with a major local Chinese OEM.

Aptiv’s long-term tailwinds are apparent.

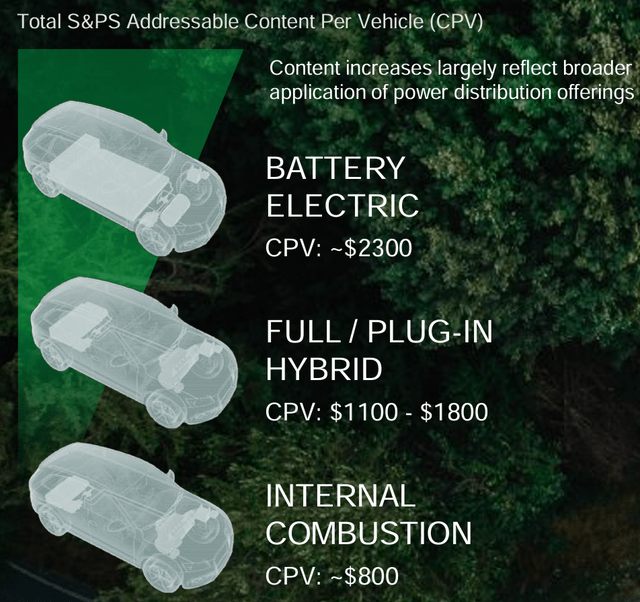

Firstly, from a content per vehicle perspective, going from ICE vehicles to hybrid vehicles brings an 80% increase in the content per vehicle, while going from ICE vehicles to electric vehicles brings an 190% increase in the content per vehicle.

Content per vehicle (Aptiv)

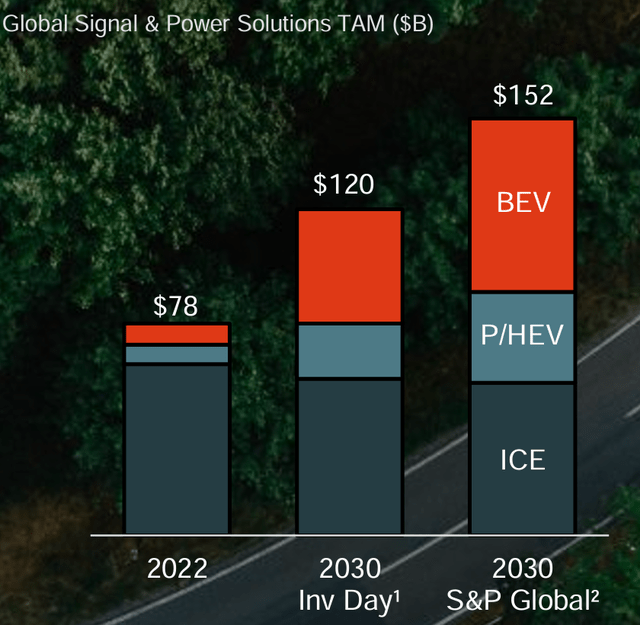

This implies that the S&PS total addressable market is expected to grow 53% on aggregate, according to Aptiv’s estimates, and even more so based on S&P Global’s estimates.

S&PS TAM (Aptiv)

Motional

This has been one of the tailwinds that I think could help rerate Aptiv given it has been a drag on earnings.

Aptiv announced in the 1Q24 quarter that it has reached a deal with Hyundai where Hyundai will buy 11% of Aptiv’s Motional stake for $448 million. In addition, Aptiv will convert 21% of its equity interest to a preferred stock holding.

This is expected to close in the third quarter of 2024.

As a result, there are direct improvements to Aptiv’s EPS due to the agreement.

Firstly, Aptiv’s common equity interest in Motional falls from 50% to 15% after the deal.

Secondly, management expects $0.30 EPS tailwind for 2024 given the transaction closes in 3Q24.

Thirdly, for the full-year impact of this deal, Aptiv sees an incremental $0.90 EPS benefit in 2025.

Naturally, this deal once executed and gone through, would make Aptiv cheaper from a P/E perspective.

In addition, it reduces the earnings drag from Motional, thereby killing two birds with one stone.

Getting the negatives out of the way

There were some pockets of weakness, although I would argue that most of that was already priced in before the earnings report.

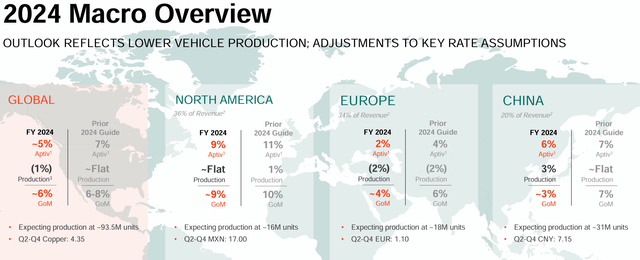

Firstly, vehicle production for 2024 was lowered from flat to -1% in the 1Q24 earnings report.

Secondly, GoM was also lowered from 7% to 6% due to slower High Voltage, electric vehicles growth.

Thirdly, all that led to the guidance being officially lowered.

Macro overview (Aptiv)

Again, I would argue that the above three points were already priced into the share price before the 1Q24 earnings, which means that now that management has officially lowered the guidance and revised the following, we have gotten the negatives out of the way.

I think it is important to note that while there was a revision downwards for the revenue for 2024, operating income margin was maintained, which implies better management execution and initiatives from the cost front.

This better cost structure and strong execution from management should give investors more confidence that even if Aptiv grows revenue in the mid-single-digit range, and if they convert at 20% incrementals, then Aptiv can still deliver $8 in EPS in 2025, which implies only 10x 2025 P/E.

Valuation

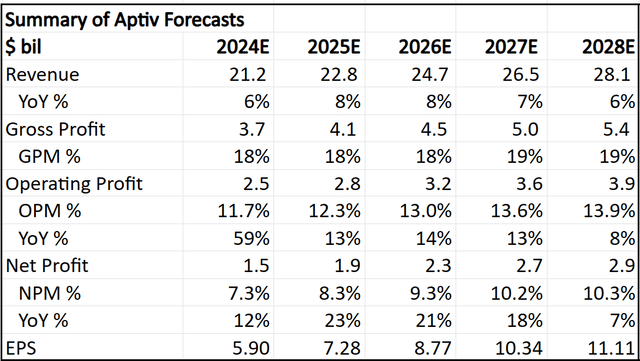

For my 2024 forecasts, I made some minor adjustments to lower the revenue down to $21.2 billion, which is at the midpoint of the new revenue guidance, adjusted operating margin up to 11.7% (slightly below guidance) and EPS to $5.90, at the low end of the guidance.

Thus, the new 2024 numbers should reflect the guidance change, Motional deal and share repurchases.

Likewise, the forecasts after 2024 needs to be adjusted for the Motional deal and share repurchases.

I estimate that the $1.5 billion in share repurchases amount to buying back 18 million shares, reducing share count by 6.5%. I am not assuming any further buybacks after 2024, although this could prove to be an upside.

Summary of my 5-year financial forecasts for Aptiv (Author generated)

As a result of these changes to the financial forecasts, my intrinsic value and price targets go up marginally.

The intrinsic value goes up marginally to $103. The assumptions used remain the same as in the deep dive article.

The 1-year and 3-year price targets also go up marginally to $118 and $158, implying 20x 2024 P/E and 18x 2026 P/E, respectively.

Conclusion

I think that the risk reward for Aptiv improves from here.

The 1Q24 was a better than feared set of results, with strong margins and in-line revenues.

With a 2024 guidance that is now lowered and thus more derisked, I think this sets Aptiv well for the rest of 2024.

We also saw some strategically important wins with the Chinese local OEMs, radar wins with a Japanese OEM, and a Gen 6 ADAS win.

In addition, the positive announcement about the Motional transaction brings direct EPS benefits to Aptiv and the accelerated buybacks will help signal that the management team sees the current price as not reflective of its true intrinsic value.

With sentiment at rock bottom before the 1Q24, I think we will unlikely see Aptiv trade at the previously depressed valuation, which was a great buy for the portfolio.

Read the full article here

2026-04-27")

")

")

")

")