2026-04-27")

")

Gilead Sciences, Foster City, CA

Gilead Sciences (NASDAQ:GILD) on Thursday announced positive topline results from an interim analysis of its Phase III PURPOSE 1 trial. The trial which tested the efficacy of twice-yearly lenacapavir versus once daily Truvada and Descovy in approximately 5,300 women at risk of contracting HIV in South Africa and Uganda, found 0 incident cases of HIV infection in the lenacapavir group. In other words, among the 2,124 treated with twice yearly subcutaneous lenacapavir, none tested positive for the HIV virus.

Some caution is warranted that the number of incident cases is small, even in a large Phase III trial. Thus, it is difficult to say if lenacapavir truly stops spread of the virus as even with thousands of participants the number of cases observed is low. However, the results are highly encouraging:

- Lenacapavir Group: Among the 2,124 women receiving twice-yearly lenacapavir, none tested positive for HIV, an incident case rate of 0.

- Truvada Group: There were 16 incident cases among 1,068 participants, an incident case rate of 1.69 per 100 person-years.

- Descovy Group: There were 39 incident cases among 2,136 participants, an incident case rate of 2.02 per 100 person-years, respectively.

Hypothetically, if the zero incident case rate held, one can imagine the dream of fully tackling the HIV epidemic within a generation. This could be accomplished through PrEP (Pre-exposure Prophylaxis) during which at risk individuals are treated preemptively, in theory reducing viral transmission to a terminal decline. As such, lenacapavir may not only be a superior HIV treatment, it also has the potential to vastly expand the market. Gilead’s stock traded over 8% higher on the news, a justified advance given that approximately 65% of the company’s revenues come from HIV product sales.

Historically, I have maintained a cautious or bearish stance on Gilead first writing in Nov 2014 that the company was at risk due to excessive concentration in two products. At the time, Sovaldi and Harvoni for hepatitis C became exposed to major competition when the stock traded slightly above $100/share. Nearly 10 years later, Gilead has become a more diversified company through expanding into oncology. With this new data strongly strengthening its HIV franchise I now consider the company a strong buy.

Franchise Diversification

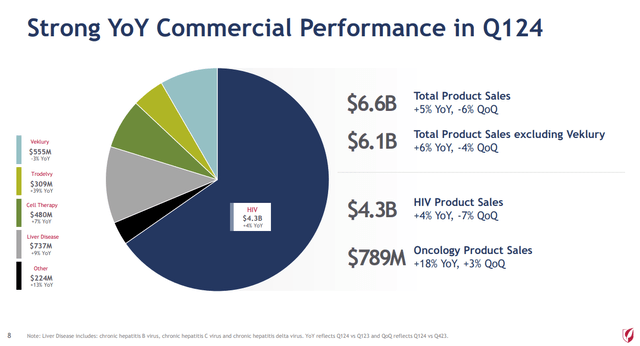

Gilead is much more diversified than in the past, with revenues coming from a mix of products in the HIV, liver disease, COVID-19 and oncology space. The following results are reported from the company’s most recent 10Q:

- HIV ($4.3 billion in sales for Q1 2024 – 65% of revenues) is led by Gilead’s leading market share in HIV PrEP treatment. Biktarvy and Descovy lead the way, with 4% growth in HIV for Q1 2024 versus Q1 2023.

- Liver disease ($737 million in sales for Q1 2024 – 11% of revenues) is led by Sofosbuvir/Velpatasvir under the brand name Epclusa in the treatment of hepatitis C. This segment is a much smaller proportion of sales than ten years prior in the days of Sovaldi and Harvoni.

- COVID-19 ($555 million in sales for Q1 2024 – 8.4% of revenues) is led by Veklury. Sales have fallen by 3% versus Q1 2023 as the pandemic has receded.

- Oncology ($789 million in sales for Q1 2024 – 12% of revenues) with growth driven by Trodelvy with 39% year over year growth ($309 million in Q1 2024 sales). The remaining revenues are derived from cell therapies resulting from Gilead’s acquisition of Kite, with Yescarta and Tecartus leading the way ($480 million in Q1 2024 sales).

Gilead Q1 2024 Earnings (Earnings Presentation – Slide 8)

In total Biktarvy is Gilead’s largest selling drug with $2.95 billion in Q1 2024 sales or 44% of revenues. The primary patent on Biktarvy will not expire until 2033, giving Gilead a long runway to improve upon its HIV franchise (see table on page 9 of Gilead’s 2023 10K report).

Growth Catalysts

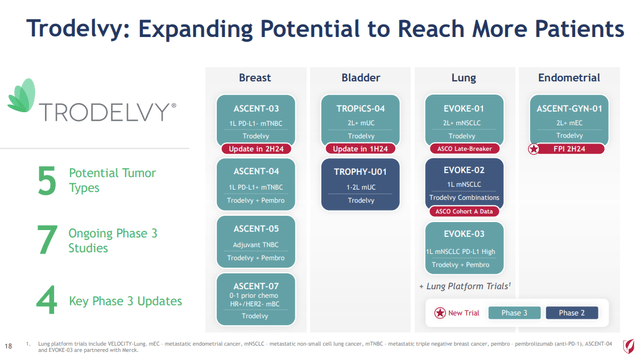

In addition to the new results in HIV highlighted above, Gilead has made exceptional progress in its oncology franchise with seven ongoing Phase III studies of Trodelvy in breast, bladder, lung and endometrial cancers.

In 2020, Gilead completed the acquisition of Immunomedics, securing the antibody-drug conjugate and since approval and commercialization has gone on a full-court press to expand markets of this promising therapy:

Expanding Trodelvy (Gilead Q1 2024 Earnings Presentation – Slide 18)

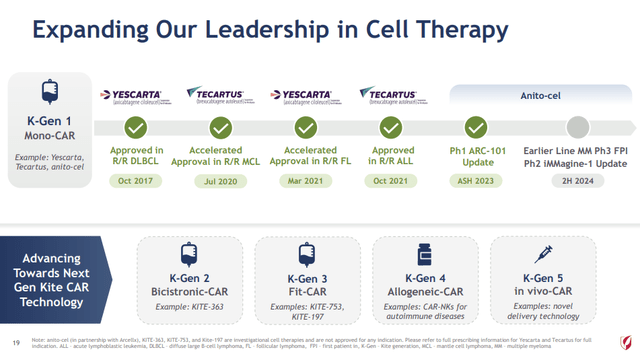

In addition, Gilead is aggressively pursuing growth in CAR-T cell therapy on the heels of its 2017 acquisition of Kite Therapeutics. Yescarta was the first CAR-T therapy approved by the FDA for relapsed or refractory large B-cell lymphoma. The company is presently advancing towards the next generation of CAR-T therapy:

Expanding CAR-T Therapy (Gilead Q1 2024 Earnings Presentation – Slide 19)

A major positive for Gilead is that the company has established inroads on several franchises: HIV, ADC oncology and CAR-T oncology. They now have drugs in each which have proven safe and effective and are expanding the number of indications and patients that can be treated by aggressively pursuing late stage clinical trials. If the company can continue to execute continued growth should be achievable.

Valuing Gilead by Discounted Cash Flow

Valuentum, a website that I subscribe to, performs an in-depth discounted cash flow analysis of many companies. Today, it could be argued based on past growth and projections that Gilead is relatively cheap.

This analysis depends on several factors, notably:

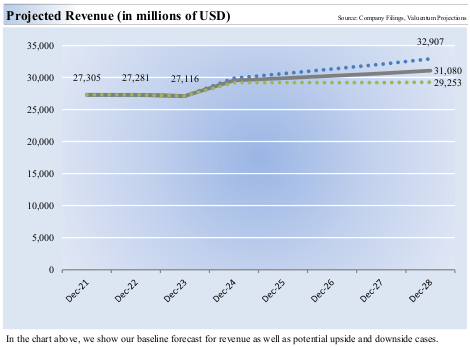

- Projected Revenue Growth: the model expects relatively limited revenue growth over the following 5 years. Gilead’s present guidance is for product sales between $27.1 and $27.5 billion for fiscal year 2024. The model projects on the low end growth to $29.3 billion over 5 years and $32.9 billion on the high end. The midpoint of this growth is 13.9% over 5 years, which seems very achievable on the basis of new products and indications within the oncology and HIV space. Management is guiding for $5.15 – $5.55 per share in 2024 earnings.

Projected Revenue Growth for Gilead Sciences (Valuentum)

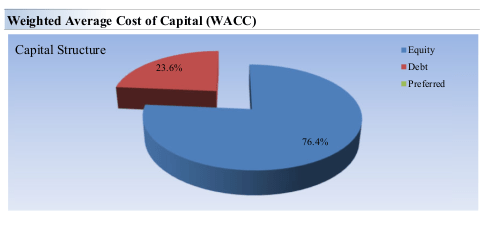

- Net Balance Sheet Impact: Gilead has increased its financial leverage over the past several years, owing to the acquisitions of Immunomedics, Kite and most recently CymaBay. However, these have returned value to investors in the form of new products. Currently, Gilead has a normalized debt/EBITDA ratio of 1.92 and 23.6% of the capital structure is debt.

Gilead Capital Structure (Valuentum)

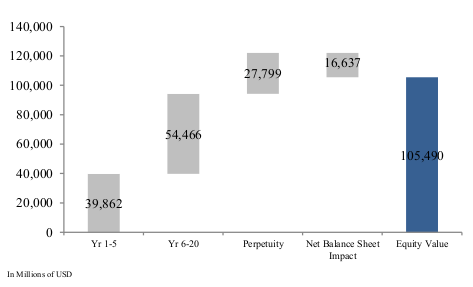

- Discount Rate: Interest rates have been rising lately and Gilead’s DCF valuation is dependent on the discount rate applied. The model applies a weighted average cost of capital of 10.2%, with a cost of equity of 11.8% and an after-tax cost of debt of 5.3%. The equity value is broken into 3 stages, with Phase I being 2.8% revenue growth over 5-years, declining to 1.4% in Phase II and 3% in Phase III.

Discounted Cash Flow of Gilead (Valuentum)

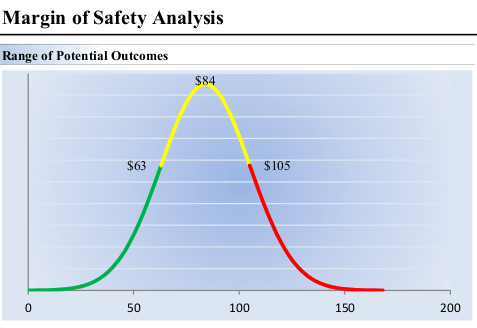

In totality, the valuation of Gilead under these assumptions is $85/share under the base case, $64/share under the lower case and $106/share under the optimistic case. Gilead also pays an attractive 4.50% dividend yield that is well covered by free cash-flow.

Margin of Safety Analysis (Valuentum)

Conclusions

The growth opportunities for Gilead within its key franchises, particularly HIV and oncology, appear to be a good deal brighter than the market is presently discounting. HIV PrEP in particular Gilead presently holds 49% market share, which may increase should lenacapavir prove to be best in class. The oncology franchise is a substantial opportunity for growth and has diversified Gilead beyond anti-viral drugs.

Over the next year, Gilead may rally on improving sentiment as these growth trends are appreciated toward a fair-value of $84/share, or 15.7x 2024 earnings guidance. In the meantime a 4.5% dividend yield is competitive with the return on cash or bonds.

The PURPOSE 1 data reported for lenacapavir represents a landmark moment in the prevention of HIV. This remarkable feat may mark a turning point in the epidemic and bodes well for the continued success of Gilead Sciences.

Read the full article here

2026-04-27")

")

")

")

")