")

")

")

")

Introduction

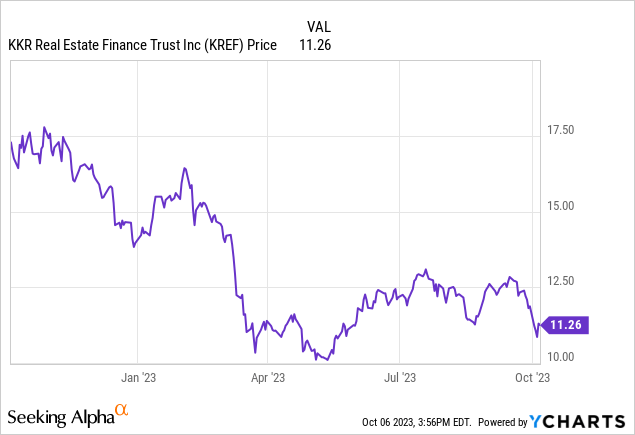

KKR Real Estate Finance Trust (NYSE:KREF) originates and invests in transitional senior loans backed by real estate. While I never really cared for the common shares of the REIT, I was interested in its sole issue of preferred shares, which are traded with (NYSE:KREF.PR.A) as the ticker symbol. Despite keeping an eye on those preferred shares I still don’t have a long position as I have been waiting to see how the REIT would be dealing with the increasing interest rates on the financial markets. Meanwhile, the share price of the preferred shares continued to slide and those preferred shares are now yielding in excess of 10%.

Checking up on the financial health of the REIT

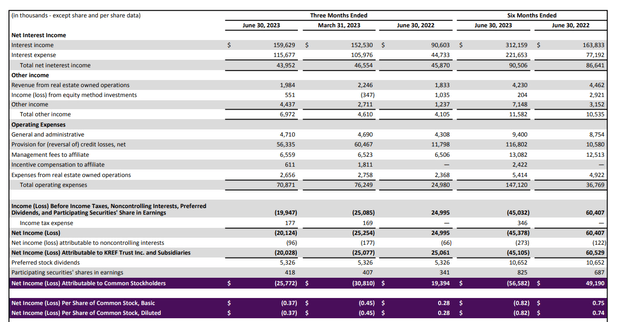

Looking at the reported net income, KKR Real Estate Finance Trust is navigating through some choppy waters as the company has been loss-making this year. Although the net interest income was still pretty decent at $44M in the second quarter, the REIT had to record in excess of $56M in loan loss provisions after already allocating $60.5M to loan loss provisions in the first quarter of this year.

KREF Investor Relations

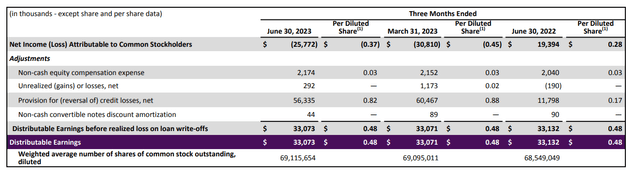

But, of course, when you’re looking at the distributable earnings, those actually do remain pretty robust. As you can see below, the total amount of distributable earnings in the second quarter was $33.07M which is almost exactly the same result as in the first quarter of the year. This means the distributable earnings per diluted share came in at $0.48.

KREF Investor Relations

While that’s encouraging and while it means the current quarterly payments of $0.43 are fully covered, the book value per share is definitely subject to erosion. By retaining just $0.05 per share per quarter, the REIT retains just over $3M in equity. That’s fine in normal circumstances. But when your loan loss provisions are consistently over $50M per quarter in the past few quarters, “saving” $3M isn’t going to be very helpful to try to protect the balance sheet.

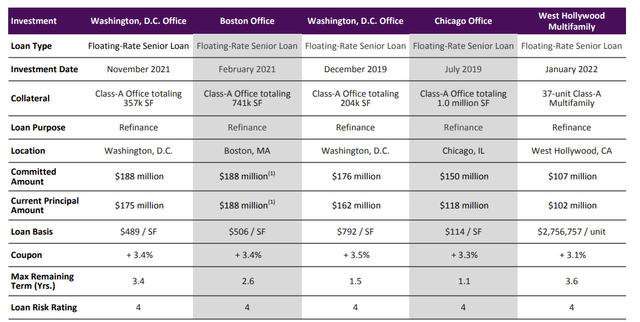

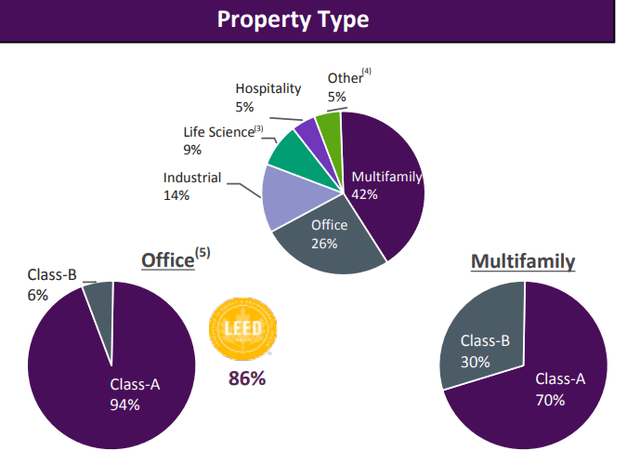

That being said, I do like the exposure to multifamily properties. One of those assets, in West Hollywood, California, has now received a risk rating of 4 by KREF. But looking at the detailed portfolio overview the $102M loan was backed by about $155M in collateral based on the 65% LTV ratio when the loan was issued.

KREF Investor Relations

Of course, property values have come down due to increasing capitalization rates, but I would like to assume it’s easier to market, remarket, and refinance multifamily properties than it is to avoid haircuts on the office portfolio.

KREF Investor Relations

The preferred shares: The preferred dividend is still covered

KR Real Estate Finance Trust has just one series of preferred shares available, and those shares were issued in April 2021. The company issued cumulative preferred shares at the normal price of $25 and with a preferred dividend yield of 6.5% which means these securities are paying $1.625 per year in preferred dividends. The preferred dividends are paid in four equal quarterly installments of $0.40625 and the preferred dividend yield will remain unchanged for as long as these securities remain outstanding.

Seeking Alpha

The preferred shares can be called by KKR Real Estate Finance Trust from April 2026 on, but given the current situation on the financial markets and the cost of capital, I don’t expect KKR to call the preferred shares, so I don’t think a yield to call perspective would be useful here.

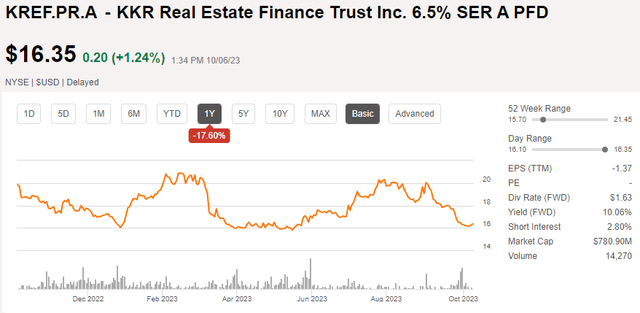

The preferred shares are currently trading at $16.35 resulting in a yield of 9.95%. That’s pretty attractive but I of course want to make sure the asset coverage ratio and the preferred dividend coverage ratio are strong enough.

Let’s start with the preferred dividend coverage level. We know the REIT was loss-making due to the loan loss provisions, but we also know the distributable earnings came in at just over $33M. Those distributable earnings already include the $5.3M in quarterly preferred dividends which means those preferred dividends are enjoying an excellent coverage ratio as the REIT needs less than 15% of its distributable earnings (before dividends) to cover the preferred dividends. So, based on that metric, the preferred shares are definitely interesting.

The main issue I have with KKR Real Estate Finance Trust right now is the asset coverage ratio. Having to deal with loan loss provisions is just part of doing business. But by not retaining a substantial amount of its earnings, there is quite a bit of erosion. In the first half of the year, the REIT had to allocate $117M to loan loss provisions while it only generated about $7M in retained earnings.

As you can see below, the total amount of equity on the balance sheet decreased by approximately $112M. Meanwhile, KKR paid out $59M in dividends on its common shares. This means that by suspending the dividend and retaining all of its distributable earnings, the REIT would have been able to reduce the impact on the book value by 50%.

Of course, suspending a dividend is not a popular move and tends to be seen as a last resort. KREF could try to launch a stock dividend while making the stock option as appealing as possible, just to try to reduce the erosion.

As you can see below, the total equity value on the balance sheet fell to $1.46B, and after deducting the $328M in preferred equity, the total value of the common equity was $1.13B or $15.07 per share. That’s already substantially lower than the $16.56 per share at the end of last year.

Fortunately for the preferred shareholders, the common shareholders are hit the hardest as they absorb those losses first. At the end of Q2, there was about $1.13B in common equity which ranks junior to the preferred shares. But at the rate of losing $100M per semester (granted, these are just loan loss provisions and provisions may be reversed), that cushion is decreasing pretty fast. Fortunately, the total portfolio size also is decreasing thanks to some repayments, and KREF is obviously actively managing its loan portfolio.

Investment thesis

The conclusion is pretty straightforward. I’m not interested in the common equity as long as the loan loss provisions are this high. I’d rather see a lower distribution and use the earnings to stabilize the balance sheet. Some investors are pointing at the excellent distributable earnings and the positive correlation between the interest rates and those earnings, but that’s a moot point if you are eroding your equity on your balance sheet. Sure, your earnings will increase, but on the other side of your equation, the value of the loans is decreasing at a faster pace than you are generating dividend income.

The preferred shares which are now yielding almost 10% are definitely somewhat safer but still speculative. A dividend cut on the common shares would be an absolute positive element for the preferred shares as it will stop or at least slow down the erosion of the equity on the balance sheet. Additionally, preferred shareholders may actually benefit from lower interest rates: They wouldn’t be impacted by the lower earnings on the common shares but the borrowers are less likely to default while the share price of the preferred shares will increase as the yields decrease.

Long story short, I’m avoiding the common shares. I currently have no position in the preferred shares but it definitely is the only security I would consider (from a speculative point of view).

Read the full article here

")

")

")

")

")

")

")

Q4 2025 Earnings Call Transcript")