")

")

")

")

Intro & Thesis

I post macroeconomic articles quite frequently on Seeking Alpha, but the last time I wrote specifically about the S&P 500 ETF Trust (NYSEARCA:SPY) was in mid-June when the underlying index was at 4,425 basis points. Since then, we have seen a sustained rally and then a correction that continues to this day. Today I would like to remind holders of SPY once again that the current correction is most likely just the beginning and it is prudent to reduce your allocation to SPY so you don’t have to wait very long for a return to previous highs.

Why Do I Think So?

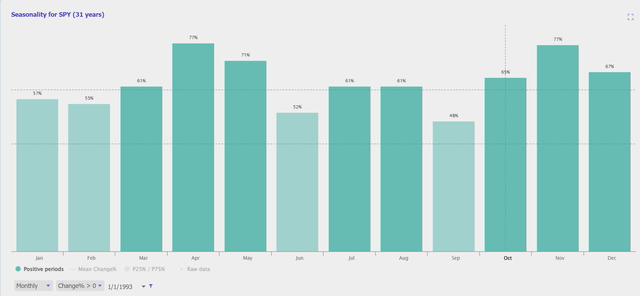

Many analysts attribute the current SPY correction to a seasonal factor. If we look at the monthly performance of SPY since 1993, we see that September is the worst month of all:

TrendSpider Software, SPY’s seasonality

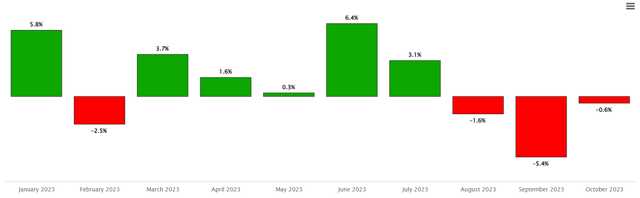

And indeed, there was a strong downward trend in September this year. However, the downward trend began in August and continues to this day, even though both August and October are median-positive, normal months.

Statmuse.com

I don’t know about you, but for me personally, justifying the price behavior of an asset based on its historical seasonality is not enough because the past does not explain the future.

Yes, after three straight months of losses, SPY may rise in November due to the effect of a self-fulfilling prophecy if the market believes in an upswing and actively buys it. But what will happen next? Let’s rely on the macro data and judge by the fundamentals.

I already wrote about this in my last article on broad market ETFs and I repeat it here: the most important thing for any economy in the world is the central bank interest rate. It is always a kind of engine for economic growth: the higher it is, the harder it is for the economy to grow and the greater the chances of avoiding overheating. Central banks balance from cycle to cycle, always warming up and cooling down the economy – that is their main task.

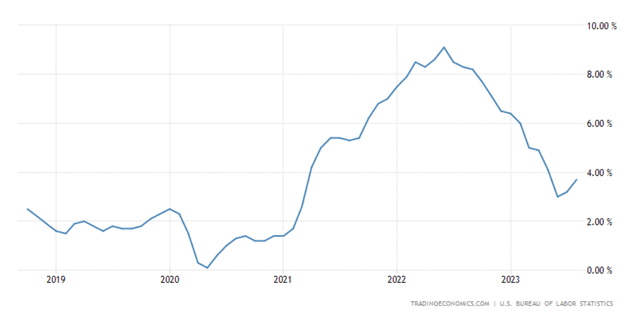

When the problem of high inflation arose a few years ago (the overheating occurred), the Fed started raising interest rates to cool the economy down again. It succeeded in doing so: Annual inflation in the U.S. fell from 9.1% in June 2022 to 3.7% in August 2023.

TradingEconomics

Interest rates remained high to prevent inflation from rising again. In turn, markets began to price in the likelihood of an imminent reversal of the Fed’s monetary policy. This led to a consensus view of good EPS growth potential against the backdrop of the assumption about the consumers’ purchasing power strength.

My macro views have long contradicted the general consensus: I don’t believe consumer purchasing power is healthy and that cloudless SPY’s EPS growth in FY2024 can somehow be justified (yes, even given the AI stuff). Upon each review of the new data, I consistently discovered indications that suggest the SPY’s EPS consensus for the next year is probably inflated.

Yardeni Research [October 4, 2023], author’s notes![Yardeni Research [October 4, 2023], author's notes](https://navarta.com/wp-content/uploads/2023/10/49513514-16965781904153612.png)

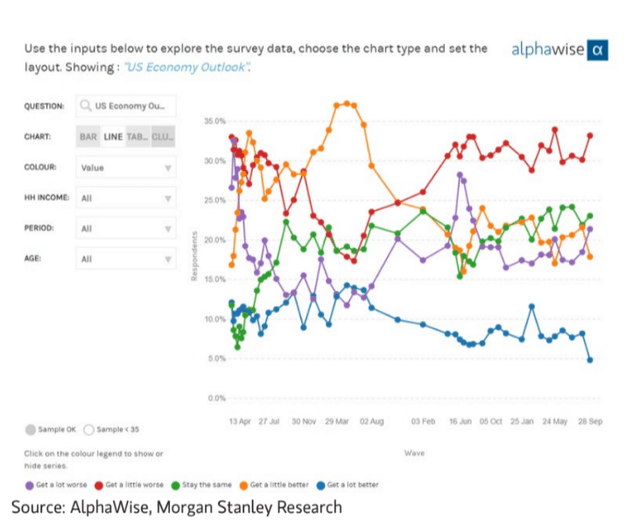

Let’s look at consumers. I like to look at indirect data, which includes surveys by Morgan Stanley’s AlphaWise analysts. Their latest survey [October 2, 2023 – proprietary source] shows that U.S. consumer confidence has declined recently: 54% now expect the economy to worsen over the next six months, up from 49% the previous month, while only 23% of consumers expect the economy to improve, down from 30% the previous month.

Morgan Stanley’s AlphaWise analysts, [October 2, 2023 – proprietary source]

I assume that everything here should work as with inflation expectations. When inflation expectations are high, economic theory says that consumers start consuming more goods before prices rise. In the case of consumer confidence, everything should work in the opposite direction: When consumers expect an economic downturn, they begin to prepare for it by adjusting their behavior (consumption) and naturally reducing it.

At the same time, according to the same study, consumers’ savings buffer fell from an average of 4.8 to 4.2 months. That is, the consumer is getting weaker, not stronger (as far as I can see) – this conclusion already casts doubt on the EPS growth Wall Street expects in FY2024.

Moreover, we have another problem that cannot yet be solved: the “risk premium imbalance,” as I call it.

You’ve probably heard without me that equities, as an asset class, began to offer a very meager risk premium sometime in 2023. For comparison, the stock market’s earnings spread to Treasuries (which by definition is the equity risk premium) is now well below spreads offered by the investment grade bond market, as the Daily Shot recently reported.

The Daily Shot [October 3, 2023]![The Daily Shot [October 3, 2023]](https://navarta.com/wp-content/uploads/2023/10/49513514-16965815720284464.png)

According to Andy Constan from Damped Spring, for SPY to adapt to the bond yields this high, it would need to reach a level of 3900. At this point, it would have the same level of risk premium as it did before the increase in bond term premiums amid anticipating today’s 12% forwarding EPS growth rate.

That is, there is some imbalance between what common sense predicts in the context of financial theory (stocks should move lower) and what is happening now (still bullish stock market views).

As Goldman Sachs macro analysts wrote in their latest research note [October 4, 2023 – proprietary source], the current interest rates setup may cause a potential slowdown in Q4 US economic growth due to tighter financial conditions, despite avoiding a government shutdown for now. Higher rates are also expected to lead to an increase in federal interest expenses and higher deficits in FY2024/25.

In the financial markets, higher borrowing costs are likely to impact S&P 500 companies’ return on equity (ROE) and pose challenges for growth stocks. And we all know exactly which stocks have become the growth drivers of SPY since the beginning of this year – these were mainly the 7 largest growth stocks in the index.

The Bottom Line

There are, of course, plenty of potential upside risks that could prove my tactical bearish call for SPY wrong. These include the possibility of positive shifts in market sentiment driven by strong economic data or favorable corporate earnings reports, central bank actions such as interest rate cuts or further stimulus measures that can boost investor confidence, and the potential for unexpected positive developments in trade agreements or geopolitical tensions easing. Additionally, market psychology and sentiment can change swiftly, leading to a reversal of current bearish trends.

However, despite the many upside risks to my thesis, I still don’t see where the double-digit EPS growth now in the consensus for FY2024 will come from. Consumers are weakening, the equity risk premium promises investors no return at best over the next few months, and interest rates continue to rise. In my opinion, this is too bad a starting point to be bullish SPY, where 28.5% is invested in techs.

So I reaffirm my Sell rating for SPY in the medium term.

Thanks for reading!

Read the full article here

")

")

")

")

")

")

")

Q4 2025 Earnings Call Transcript")