")

My Thesis

I last wrote about Sibanye Stillwater Limited (NYSE:SBSW) in March 2023, when it was priced at just over $8 a share. So as you can see, the stock has fallen more than 20% since then (as measured by total return), making my earlier buy recommendation wrong, as the market has rallied more than 9% over the same period.

Seeking Alpha, the author’s previous take on SBSW stock

The potential recovery in automotive demand did not materialize (as did some other factors) and prices for key metals for SBSW continued to fall – since the publication of my last article, palladium prices have fallen 16.3% and platinum 4.9%, according to Johnson Matthey. Only gold has gained 4.6% in that time, which obviously, turned out to be insufficient. In addition, Sibanye Stillwater’s costs have risen in recent months due to factors such as inflation, supply chain disruptions, and labor unrest – putting pressure on the company’s margins, and making SBSW’s low valuation multiples irrelevant.

But as they say in the world of long-term investing, you need to be greedy just when everyone is fearful. After evaluating the company’s situation and based on likely industry trends over the next few years, I reiterate my earlier buy recommendation and see SBSW bottoming relatively shortly.

My Reasoning

First off, a few words about the firm.

Sibanye Stillwater is a South African mining and metals processing group with a diverse portfolio of projects spanning five continents. They are among the world’s largest recyclers of platinum group metals (PGM) from auto-catalysts and have controlling interests in mine tailings retreatment operations. Sibanye produces platinum, palladium, rhodium, gold, ruthenium, nickel, chrome, copper, and cobalt, securing various revenue streams.

As The Value Corner, fellow Seeking Alpha analyst wrote in his June article, Sibanye has a wide economic moat that is built on its extensive mining and processing operations, including battery metals, and its global geographic reach. Initially a South African gold mining company, it has expanded through acquisitions and diversification, reducing its reliance on gold prices for profitability. The acquisition of the U.S. PGM business Stillwater has proven crucial for geographical diversification and stability. To date, Sibanye holds controlling stakes in international mining and processing operations, diversifying into “green metals,” such as lithium and nickel, which are used in decarbonization projects. The company’s diversified portfolio across a wide geographic area helps mitigate risks associated with relying on a single commodity or market, particularly in South Africa’s complex political environment.

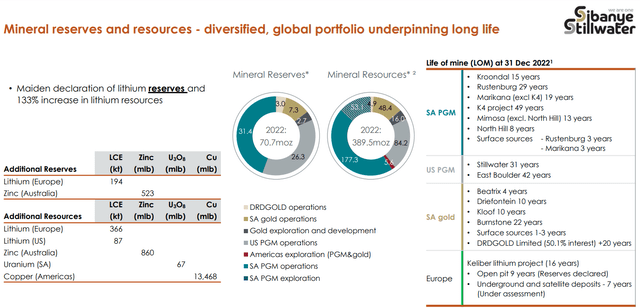

Anyway, the company’s largest revenue segment is South African underground PGM operations – this is the company’s largest resources base of all segments:

SBSW’s IR materials

Despite the challenging economic environment and potential price weakness, the SA PGM operations were well-positioned to continue performing with only a 9% cost increase in 1H FY2023, which was lower than their peers, SBSW’s management noted during the latest earnings call.

Overall, PGM operations maintained solid performance, producing 799,182 ounces of platinum, palladium, rhodium, and gold (4E). There was a 3% decrease in production year-on-year, but this was planned due to the closure of the Simunye shaft. While all-in sustaining costs (AISC) for PGM operations rose to R19,716 per ounce of 4E, a 9% increase from the previous year, the company highlighted that their operations were steadily moving down the industry cost curve and gaining a competitive edge in terms of cost margins.

In their SA gold operations, Sibanye-Stillwater reported significant improvement, with a 117% increase in gold production during the first half of the year. They also highlighted a 22% increase in the rand gold price received, demonstrating the countercyclical value of gold during economic downturns. However, they faced challenges such as a fire incident and seismicity, particularly at the Kloof 4 Shaft.

The Recycling segment confronted multiple challenges during H1 2023, as a diminishing global collections network, dwindling 3E PGM basket prices, rising interest rates, and persistent recession concerns created a turbulent environment. U.S. PGM recycling operations were notably impacted, witnessing a substantial 55% decrease in volumes compared to the same period in 2022. Adjusted EBITDA for the Recycling segment also felt the pressure, plummeting by 49% year-on-year to $20 million (or ZAR 371 million), yielding a margin of 5%. This downturn was primarily attributed to a 6% reduction in the 3E PGM basket price to $2,735 per 3E ounce, coupled with a substantial 58% decline in 3E PGM ounces sold, which totaled 153,446 3E ounces.

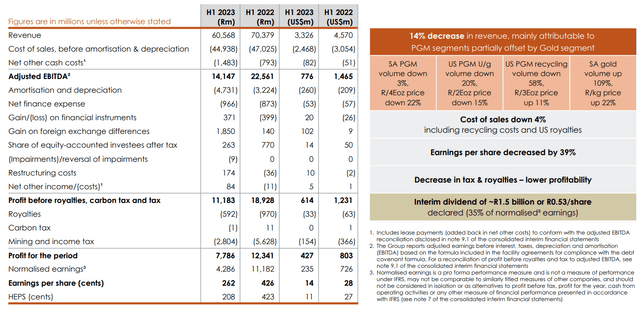

Overall, SBSW’s revenue for H1 2023 was $3.33 billion, representing a 14% decrease compared to the same period in 2022 when measured in the South African rand (when converted to USD, this decline amounted to 27%). SBSW’s EBITDA for H1 2023 was $776 million, reflecting a 37% decrease in the South African rand compared to H1 2022 (in USD terms, this decline was 47%).

SBSW’s IR materials

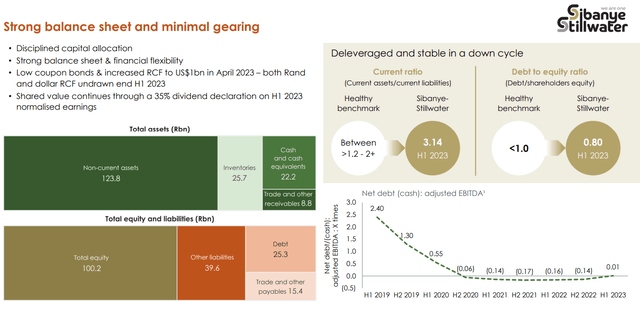

With all this negativity, it’s worth noting that the company’s balance sheet looks very strong, with a very high current ratio and a fairly low debt-to-equity ratio – the cash on the balance sheet alone is almost as high as the debt.

SBSW’s IR materials

The company aims to maintain a marginal net debt position, but some increase in net debt to EBITDA may occur as expenditure on projects increases (but not higher than 1x, according to the earnings call commentary).

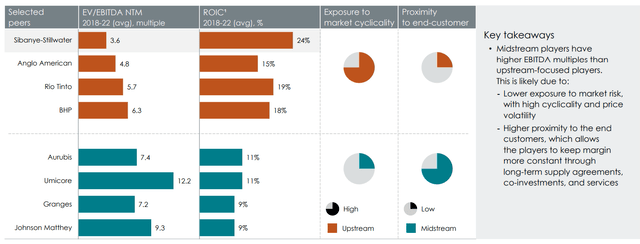

By now, it’s clear to everyone that the industry in which SBSW operates is in decline, and the current downcycle has been going on even longer than most thought (including myself). But if we zoom out a bit and look at average ROIC and valuation, SBSW has looked quite stable in this regard in the past:

SBSW’s IR materials

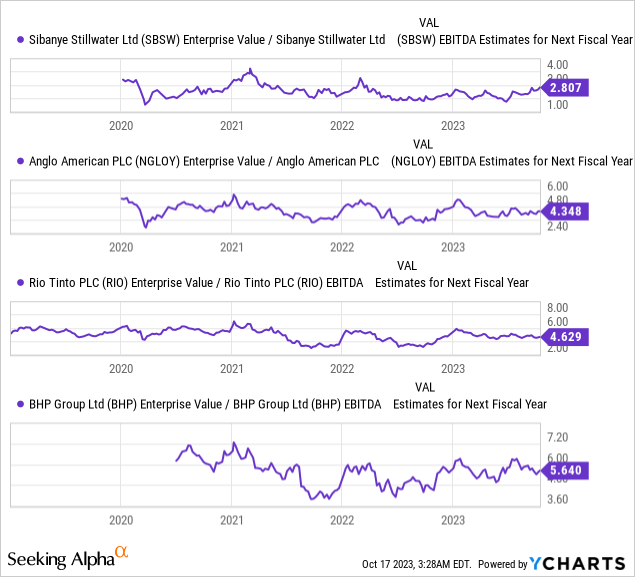

Moreover, as we saw from the balance sheet data above, SBSW has remained operationally stable to date, despite some idiosyncratic incidents and a sharp drop in the price of key commodities. Furthermore, if we compare the current enterprise value with the projected EBITDA figures of the peer group above, we see that SBSW’s EV/EBITDA deviates strongly from its historical average and is below 3x, which is significantly lower than the peer group.

Now everything depends on how the prices for commodities and thus the demand for them behave. The company expects OEMs’ destocking to take several quarters before prices stabilize and improve, particularly for metals like rhodium, anticipating a couple of quarters to go for the market to wash out the excess stocks.

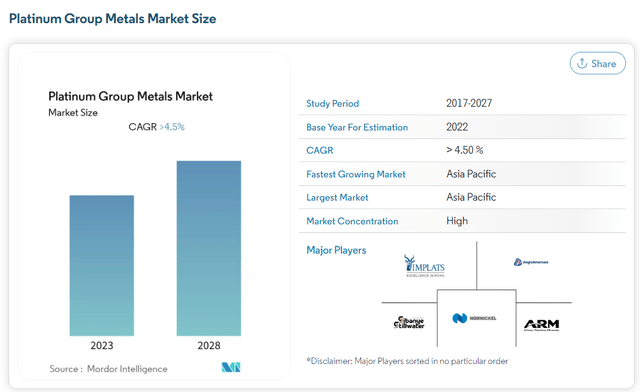

According to Mordor Intelligence, the PGM market is projected to grow steadily, with a CAGR of over 4.5% during the forecast period [2023-2028]. Although the COVID-19 pandemic had a negative impact in 2020, the market has since recovered and is expected to continue growing.

Mordor Intelligence

Short-term factors driving this growth include increased demand for catalytic converters from the automotive industry and rising needs for platinum, palladium, and ruthenium in the electronics sector. While high maintenance costs pose a challenge, the market may find new opportunities in the future through growing research and development in the electronics sector and increased investments in African countries for platinum group metals. The Asia-Pacific region is expected to dominate the market and exhibit the highest growth rate during the forecast period, the analysts wrote.

Sibanye’s PGM division also may gain synergies through potential involvement in the PGM tailings sector. As another Seeking Alpha fellow, Pearl Gray Equity and Research, noted recently, rumors suggest that SBSW’s subsidiary, DRDGold, is considering entry into this sector. While the specifics are complex, DRDGold’s CEO expressed interest in this endeavor. A partnership in PGM tailings could bring cost synergies to Sibanye and strengthen its financial statements. While DRDGold’s operational independence currently involves proportional consolidation, a 50% recognition would be highly advantageous for Sibanye. With various ancillary businesses linked to its core operations, such as tailings and PGM recycling, Sibanye-Stillwater is poised to gain a competitive edge in the future.

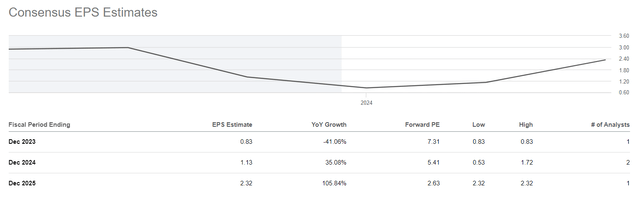

When I evaluate management’s forecasts and compare them to third-party research, I understand that Wall Street’s forecasts for SBSW’s earnings per share, at least for fiscal 2025, look pretty realistic:

Seeking Alpha, SBSW Earnings Estimates

At the current share price, the implied P/E ratio for FY 2025 is only 2.6x, which is extremely low and probably not sustainable (in a good sense for shareholders).

The Risks Factors

Sibanye faces significant risks despite its growth prospects. One of these is South Africa’s chronic power supply problem. Frequent power outages disrupt operations and pose a significant revenue risk.

Another issue is the demand for Sibanye’s raw materials, which is dependent on global trends. Although these trends look robust in the long term, the short-term economic forecasts remain uncertain. South Africa’s unstable political environment could deter foreign investment and affect Sibanye’s valuation.

From an ESG perspective, unethical practices could lead to labor issues.

Rhodium price volatility is a risk, although the 4E basket provides a buffer. Palladium is threatened by the increasing penetration of electric vehicles.

Recycling presents a short-term challenge but promises long-term potential. The lithium project involves significant investments and takes time to pay off.

Your Takeaway

Despite industry challenges, I think that SBSW maintains a strong balance sheet, and its focus on platinum group metals recycling and expansion into “green metals” positions it well for long-term growth. The potential entry into PGM tailings recycling could further enhance its financial strength, offering potential benefits for investors. While the short term has seen difficulties in certain segments, Sibanye’s resilient performance, low valuation relative to peers, and anticipated recovery in commodity prices make it an appealing investment option in the long term.

That’s why I reaffirm my previous Buy rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q1 2026 Earnings Call Transcript")

")

")

")

")

")