")

A true conservationist is a man who knows that the world is not given by his fathers but borrowed from his children.” – John James Audubon

Today, we take a look at a small-cap firm targeting various industrial end markets. The company is diversifying away from its legacy oil & gas and power generation into these end markets to make it less cyclical. All of its business lines are producing strong results with management raising its FY23 outlook three times since its first forecast in November 2022. With record orders and backlogs but higher interest expenses from a recent acquisition spree, the recent insider buying merited further investigation. An analysis follows below.

Seeking Alpha

Company Overview:

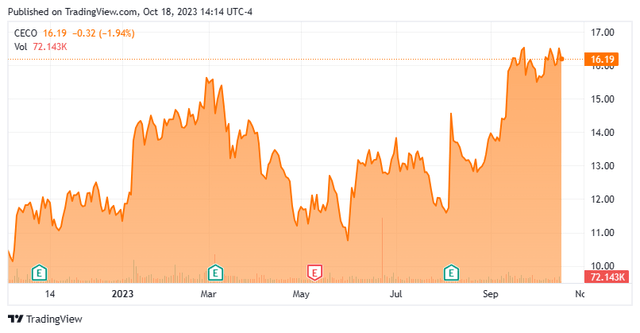

CECO Environmental Corp. (NASDAQ:CECO) is a Dallas-based supplier of air and water quality solutions to a wide range of industrial end markets, broadly characterized as industrial air, industrial water, and energy transition. The company boasts an “installed base of more than 32,000 air pollution control systems with the capability to eliminate more than 4.4 billion pounds of pollutants per year, equivalent to removing more than 50 million passenger vehicles from the road.” With roots dating back to 1869, CECO was formed in 1966 as Claremont Engineering and now employs ~1,000 individuals in nine countries, serving nearly 900 customers across 11 major verticals. The stock trades at just over $16.00 a share, translating to an approximate market cap of $570 million.

August Company Presentation

Operating Segments

The company views its operations through two segments: Engineered Systems and Industrial Process Solutions.

Engineered Systems provides emissions control, fluid bed cyclones (for heavy oil refining), noise abatement, separation, and filtration, as well as dampers and expansion joints to the power generation, hydrocarbon processing and transport, water treatment, and shipbuilding industries. The unit generated FY22 income from operations of $36.2 million on revenue of $263.2 million versus income from operations of $25.8 million on revenue of $186.9 million in FY21.

Industrial Process Solutions provides air pollution and contamination control, fluid handling, and filtration solutions for a wide range of verticals, including aluminum cans, automobiles, food and beverage, steel, wood manufacturing, desalination, aquaculture, electronics, and semiconductors. The segment produced FY22 income from operations of $22.7 million on revenue of $159.4 million versus income from operations of $15.1 million on revenue of $137.2 million in FY21.

Approach

Prior to the onboarding of CEO Todd Gleason, CECO was perceived as a cyclical concern tethered primarily to the oil & gas and power generation verticals. The company has since endeavored to diversify into other end markets with an emphasis on industrial air and water solutions, aided by acquisitions, executing six deals since the onset of 2022. Management expects at least four of them to double in size over the first 18 to 24 months under CECO. That said, 81% of the $98.5 million in revenue growth it achieved FY22 vs FY21 (up 30%) was organic as it benefitted from upticks in its legacy businesses.

In addition to attempting to ride ESG-generated secular tailwinds, the company is expanding internationally into high-growth markets, particularly Asia from the Mideast and to its eastern shores.

Despite its recent top-line success, like many industrial concerns, CECO has experienced margin compression due to inflationary pressures on materials and labor with gross margin falling from 33.3% in FY20 to 31.1% in FY21 and further to 30.3% in FY22. To combat this COGS pressure, management has prioritized booking higher-margin, short-sales cycle projects with a goal of generating half its top line from these deals (currently ~30%) over the long term.

2Q23 Financial Report & Revised Outlook

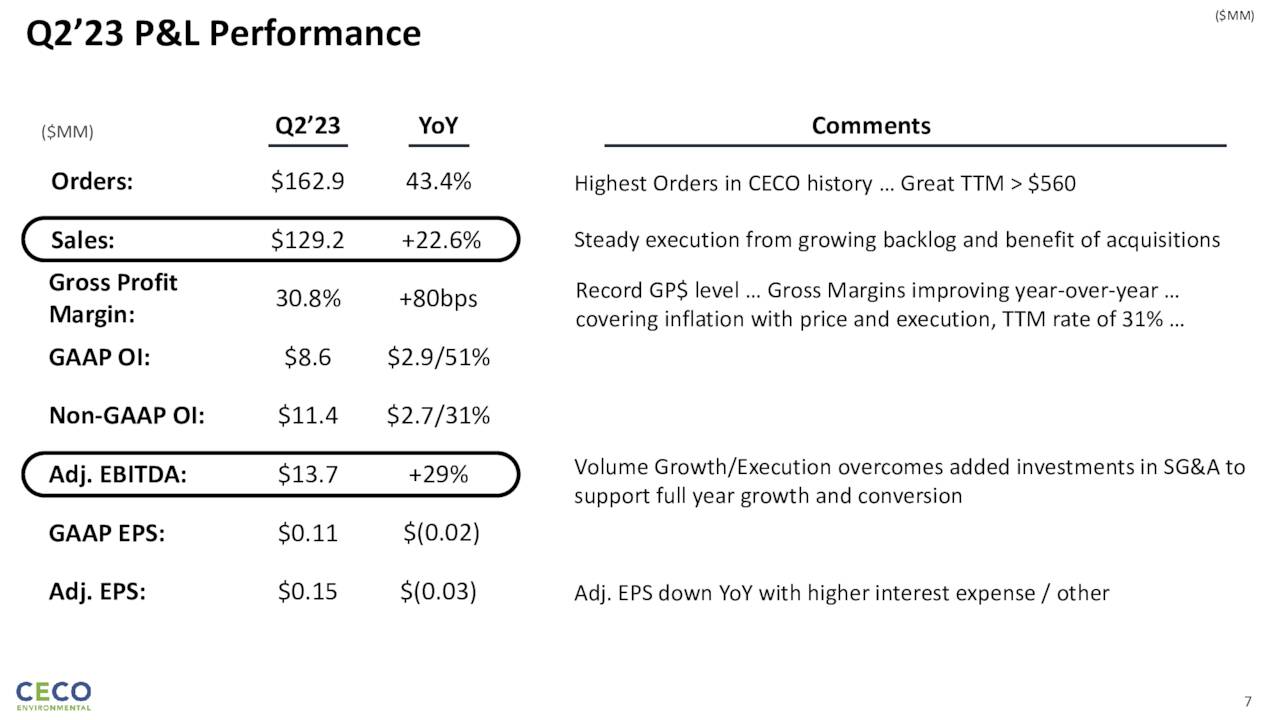

Management’s pivot appears to be paying off, based on most measures reported in its 2Q23 financials announced on August 8, 2023. CECO posted earnings of $0.15 a share (non-GAAP) and Adj. EBITDA of $13.7 million on net sales of $129.2 million versus $0.18 a share (non-GAAP) and Adj. EBITDA of $10.6 million on net sales of $105.4 million in 2Q22, representing increases of 29% and 23% at the Adj. EBITDA and revenue lines (respectively), which were both records. However, higher interest expenses led to a 19% decline at the non-GAAP bottom line ($5.2 million versus $6.4 million) – more on that shortly. Against Street consensus, non-GAAP earnings were in line, while revenue beat by $11.4 million. Growth at the top line was not all acquisition-related but across the board, with 16% of the 23% growth organic.

August Company Presentation

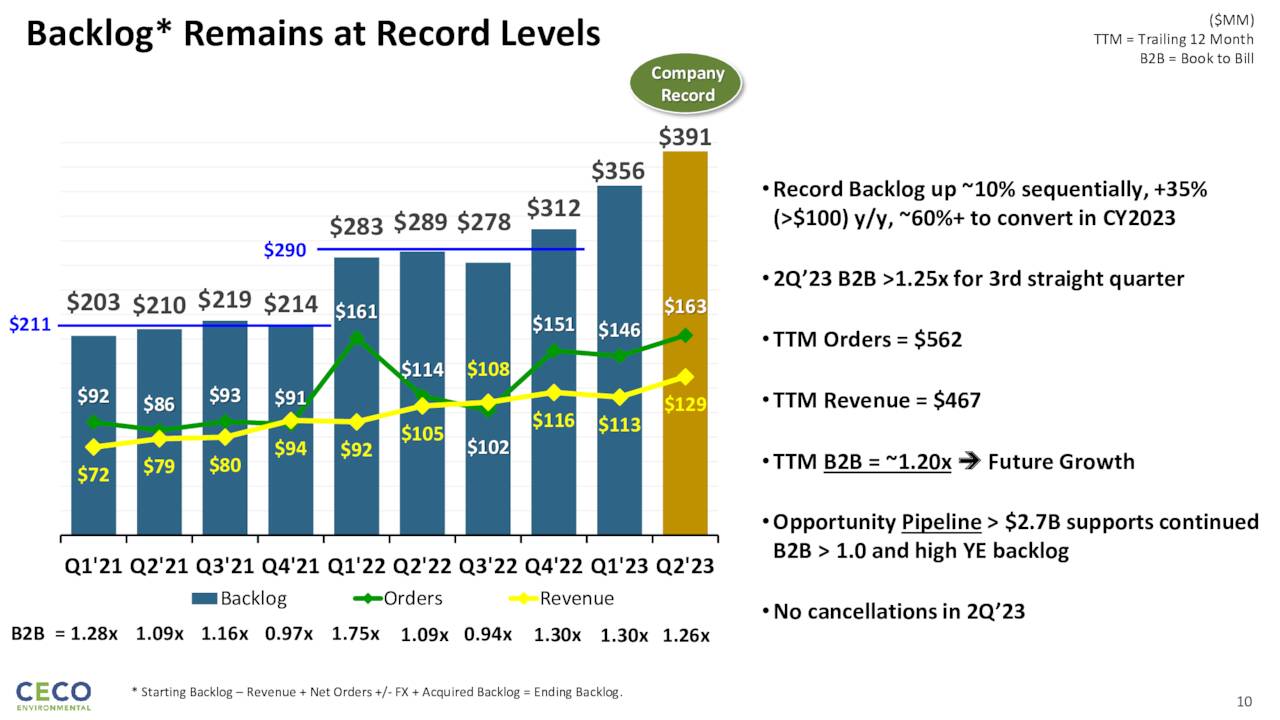

Other metrics showed strength: gross margin improved 76 basis points to 30.8% – albeit down 18 basis points sequentially; Adj. EBITDA margin rose 55 basis points to 10.6% (up 199 basis points sequentially); orders in the quarter were a record $162.9 million, up 44% year-over-year; backlog grew 35% to a record $391.0 million; and CECO’s book-to-bill ratio was a robust 1.26 – its third consecutive quarter above 1.25.

August Company Presentation

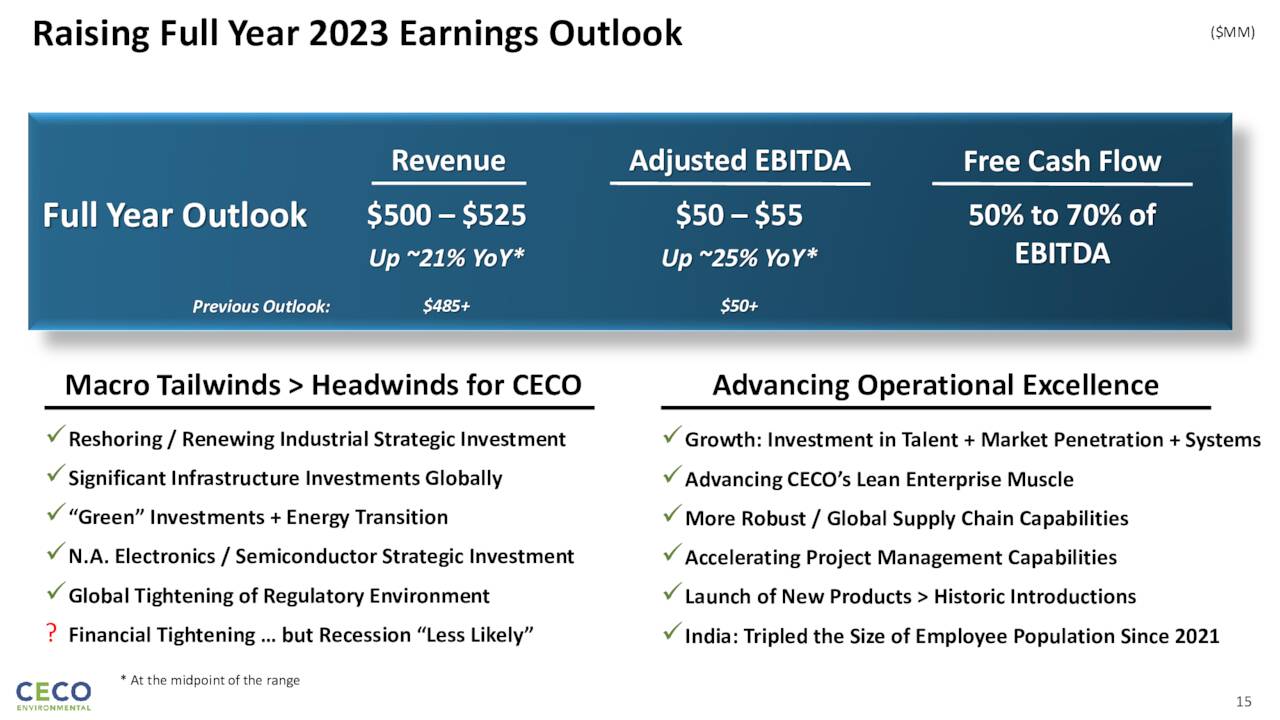

On the back of the strong stanza, management raised its FY23 outlook for a third time since its first forecast in November 2022. Based on range midpoints, CECO is now expected to generate Adj. EBITDA of $52.5 million on revenue of $512.5 million, up from its initial projections of $46.5 million on revenue of $462.5 million. Certainly, the acquisition of new businesses has contributed to its routinely raised outlook, but the company is clearly executing its transformation plan with ~$100 million of its FY23E top line derived from high-growth markets in Asia, more than double that generated in FY22.

August Company Presentation

The market liked the report, rallying shares of CECO 24% to $14.56 in the subsequent trading session but below a nine-year high of $16.73 achieved in March 2023. The equity has added to that one-day rally since.

C-Suite Transition

Despite the solid report and momentum, it should be noted that the company has terminated its relationships with its (now former) Chief Operating Officer and Chief Accounting Officer, both announced through 8-Ks in July 2023. The circumstances around their dismissals were not further elaborated upon and not brought up on the 2Q23 conference call. A replacement for the CAO has been announced but not the COO.

Balance Sheet & Analyst Commentary:

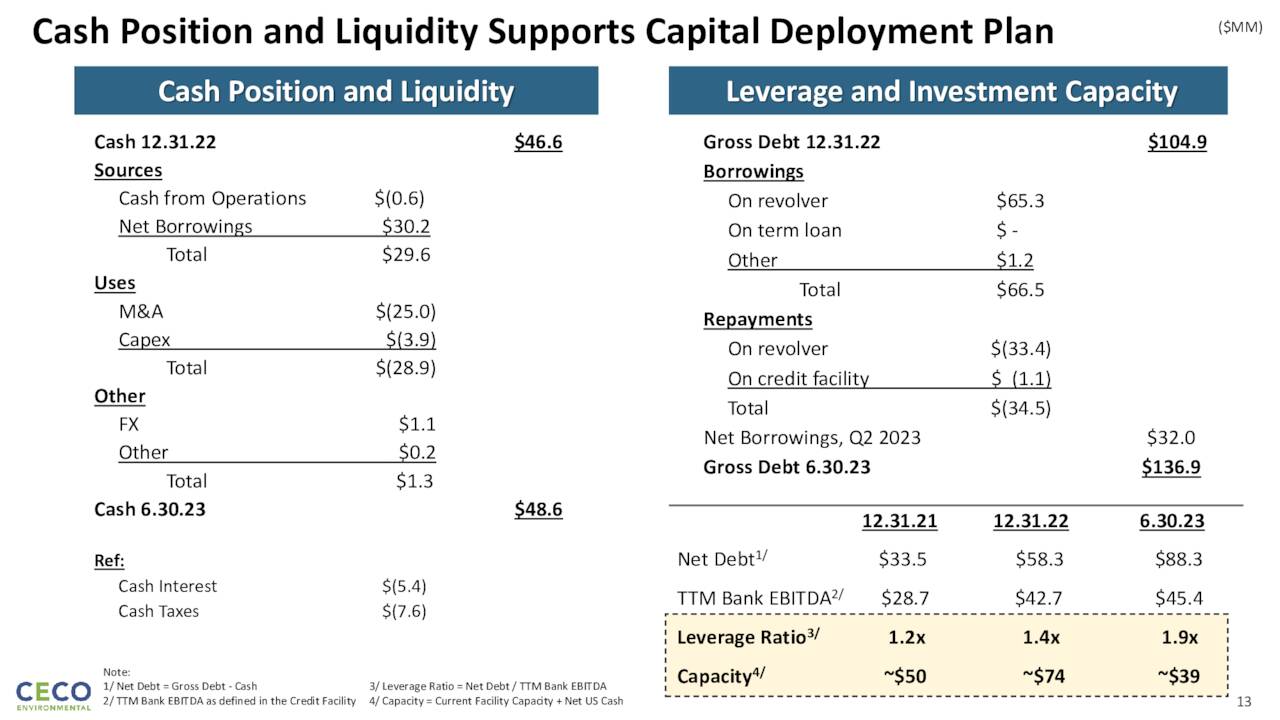

To finance acquisitions that allow it to grow beyond its legacy businesses, CECO has leveraged its balance sheet, raising debt from $63.8 million to $141.6 million (and its leverage ratio from 1.2 to 2.1) in the 18 months ending June 30, 2023. On that date, it held unrestricted cash of $47.6 million with another $26.4 million available on a credit facility. While executing its transformation plan, the company did not pay a dividend but did approve a $20 million share repurchase program in May 2022, of which it has $13.0 million remaining under its authorization.

August Company Presentation

Street analysts unanimously appreciate CECO’s expansion of its addressable markets, both from an industrial end-user and geographic perspective. They feature five buy ratings and a median twelve-month price objective of $21. On average, they expect the company to earn $0.65 a share (non-GAAP) on net sales of $515 million in FY23, followed by $0.91 a share (non-GAAP) on net sales of $554 million in FY24, representing gains of 41% and 7%, respectively.

Board member Richard Wallman is also constructive, purchasing 22,000 shares in September of this year.

Verdict:

With its focus on being perceived as a less-cyclical concern, CECO is clearly on an upward trajectory, rendering an investment decision predominantly a function of value – the recent upheaval in the C-suite notwithstanding. Based on Street forecasts, it trades at a PE ratio of 25 on FY23E EPS and 18 on FY24E EPS; a price-to-sales of 1.1 on FY23E revenue, and just over 1 on FY24E revenue. On an EV/TTM Adj. EBITDA basis, the company trades at under 13. Given its gross margin profile in the low 30s, none of these metrics are terribly compelling. However, the bet is that it will outperform Street estimates, making these metrics more attractive. As such, a small starter position seems warranted at current levels.

This book was written using 100% recycled words.” – Terry Pratchett

Read the full article here

Q1 2026 Earnings Call Transcript")

")

")

")

")

")