")

2026-05-13")

Small caps, big returns – May 2025

Dear Partners,

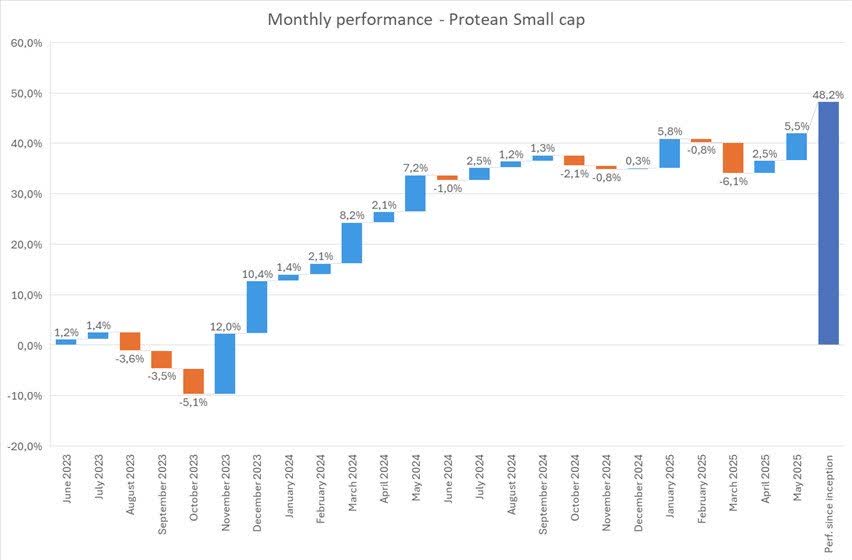

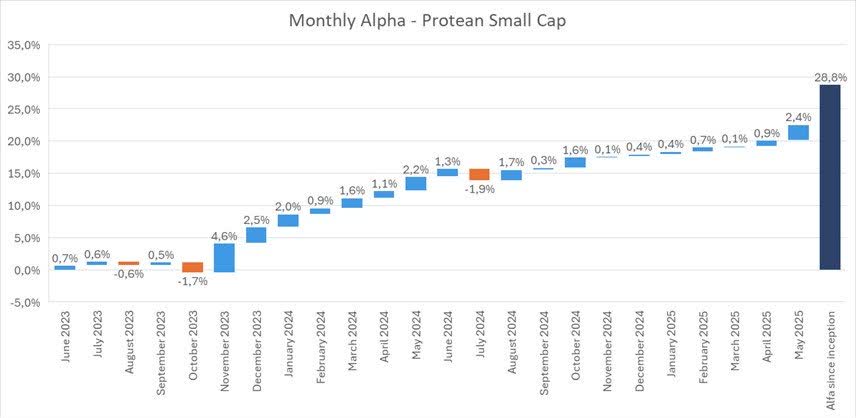

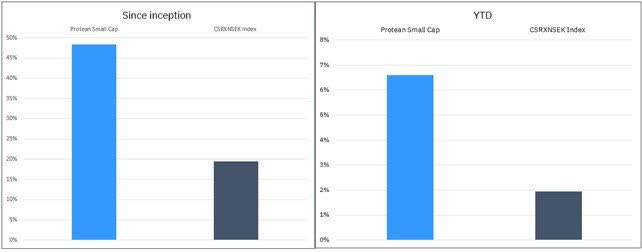

Protean Small Cap returned 5.5% in May, outperforming its index by 2.5% points. Since launching in June 2023, it has gained 48.3%, which is 28.8%-points ahead of the Carnegie Nordic Small Cap Index.

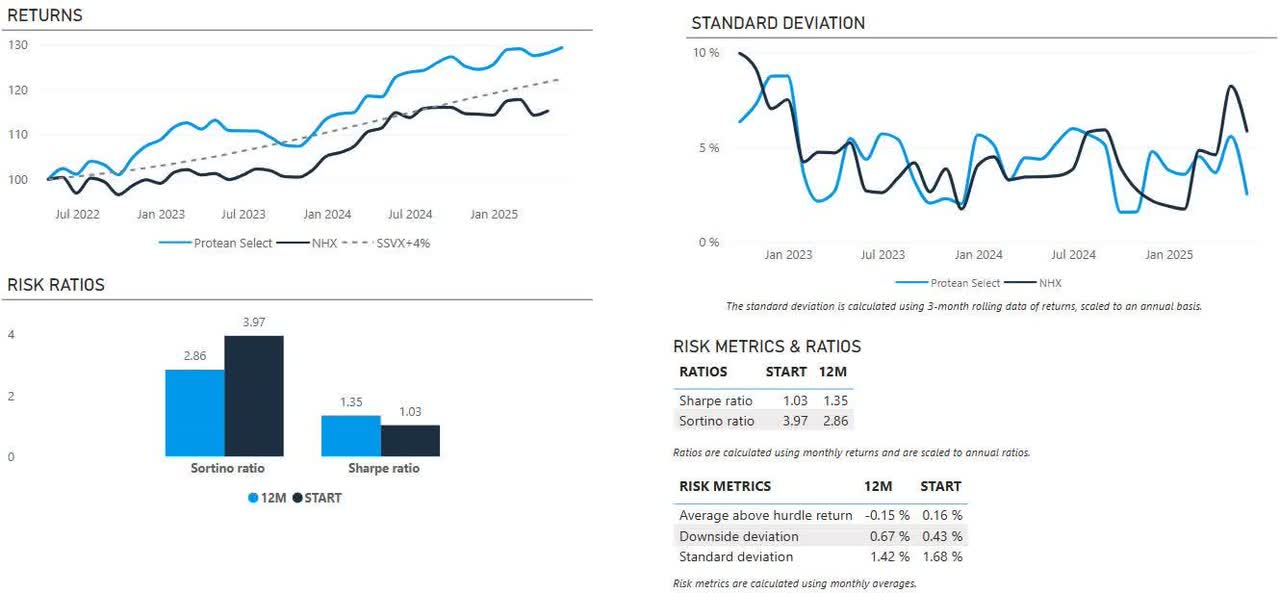

The hedge fund Protean Select returned 0.9% in May, staying true to its objective of generating reasonable returns and avoiding large drawdowns. Year to date the return is 3.0%.

Protean Aktiesparfond Norden, our recently launched fund that combines the low fees of passive funds with the active fund’s chance of beating the market, continues to do what we hoped it would do: outperform. Since inception two months ago it is up 6.8%, that is 4.1%-points ahead of the index (VINX Nordic Cap SEK). It now manages >500m SEK.

This month’s letter elaborates on the first two successful years of Protean Small Cap, why we think beaten-down Arjo (OTCPK:ARRJF) deserves a second (or third) look, why Investment Companies have had their day in the sun. And, as always, a handful of other stock observations and commentary.

Thank you for being an investor!

// Team Protean

Protean Small Cap (Carl’s update for May)

Protean Small Cap returned +5.5% in May. That is 2.5% points ahead of the CSXRN (SEK) benchmark index for the month. This puts the fund 28.8% points ahead of our index (CSRXN SEK) since inception, and performance since start is 48.3%. The fund now manages ca. SEK 600m. Thank you for your trust.

Two years running

We celebrate two years as a fund! So far so good, we can conclude. We have gotten off to a good start in terms of both absolute and relative performance.

We appreciate the trust we have gotten so far, as there’s no shortage of small cap funds in the Nordics. The fund started with SEK 60m, which has growth to ca. 600m as we enter June.

We felt that we needed to bring something new to the table when we launched Protean Small Cap. Instead of launching another generic fund with the stated objective of being a ‘long-term investor in quality companies’, we have chosen another approach: we will be opportunistic and focusing on risk/reward in each individual situation we engage in. This leaves us vulnerable to setbacks in individual stocks, but in aggregate we believe we have a higher base return in the portfolio relative to our benchmark. We avoid concentration risk, rarely having a position weighing more than five percent. If it’s above that threshold, this is due to performance, and we are likely to reduce the size when appropriate.

We believe we have a higher portfolio turnover, which (apparently) is somewhat controversial to some. Everyone loves to mention how long-term their investment horizon is, and sure, we have a five-year horizon in our investments as well. However, fundamental, unpredictable things happen, share prices move and alternative investments emerge.

Had we kept our starting portfolio from May 2023 unchanged, it would have returned roughly 30 percent until today. Marginally better than the benchmark, but a far cry from the actual 49 per cent we have achieved so far. Investment is a marathon, not a sprint, but each step matters. To us, resetting the performance to zero and starting every month fresh helps us keep focused on keeping a good pace and constantly look for new ideas and re-evaluate our portfolio.

Looking at the historical data, a remarkable feature we note is that over 24 months, the fund has underperformed the benchmark only three months. The chart above is simply performance vs the Carnegie Nordic Small Cap Index (in SEK and net of fees). We do not manage for monthly returns, but every month counts.

To maximize the opportunity, we needed to cap the size of the fund. To be able to trade without an outsized market impact, a real small cap fund can’t grow too big.

We still have ample room to grow to SEK4bn, which we consider to be a level where we can still use this mindset to create attractive returns.

Here’s to hoping it continues.

May re-cap

Main contributors in May were Pexip (OTCPK:PXPHF), Asmodee, Rugvista, Acast (OTCPK:ACASF) and Ratos (OTCPK:RTOBF). The Norwegian software company Pexip gained 51 percent during the month as the strong performance of their self-hosted video communication software in the defense vertical was brought to wider attention. Asmodee’s quarterly report beat expectations by a mile, which increased trust in this recent spin-off from Embracer, which we spoke about in the February letter. Rugvista gained 29 percent on the back of a strong Q1 report, which showed a return to double-digit organic growth, a solid gross margin expansion of 240 bps while they also were able to scale on marketing investments.

Acast is on the verge of a tipping point for their North American operations, which grew by 65 percent in Q1. The report strengthened our belief that we are witnessing an inflection, with profitability being achieved for the full year 2025.

Detractors include ITAB, Ework, Meko, Arjo and Embracer (OTCPK:THQQF). ITAB swung back from a strong performance during April. Ework fell sharply after posting earnings that showed a surprisingly large decline in activity in Q1, which partly can be explained by their increased focus on more value-added services.

We have added Hexpol (OTCPK:HXPLF) and Billerud (OTCPK:BLRDY). Both these two industrials offer reasonable valuation, strong balance sheets and have performed better operationally than what their share prices suggest. We also added Sinch (OTCPK:CLCMF). This communications provider has improved their cash flow generation, taken down debt quickly and the combination of a return to organic growth, improved operational performance and (we believe) upcoming buybacks is not captured in the valuation. We have also increased our weights in Nilfisk (OTC:NLFKF) and RTX, two portfolio laggards that have shown promising signs recently.We have sold our stakes in AAK (OTCPK:ARHUF) and Huhtamäki (OTCPK:HOYFF).

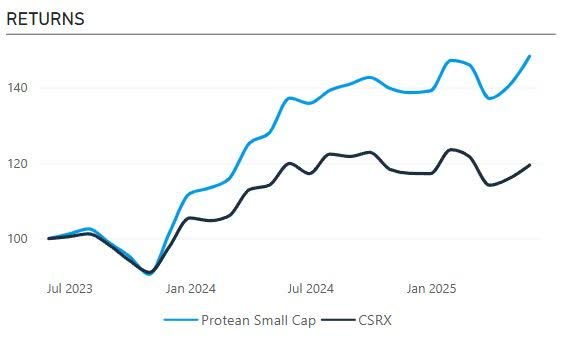

Protean Small Cap vs Index since inception

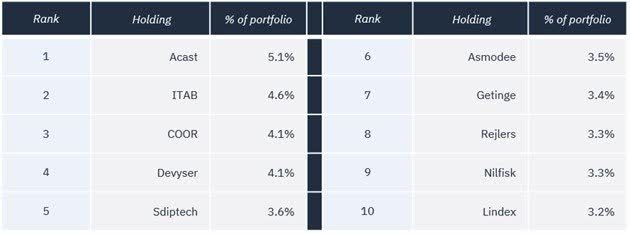

The ten largest positions in Protean Small Cap as we enter June:

Protean Select (Pontus’ update for May)

| *We illustrate our performance by showing a comparison with the NHX Equities index. This is an index constructed from the performance of 45 Nordic hedge funds focusing on equity strategies. NHX is published after our Partner Letter, so updates with one-month lag in the chart above. We aim to have positive returns regardless of the market, but no return is created in a vacuum, and a net-long strategy will correlate. Our hurdle rate is 6.3275% annualized (4% + 90-day Swedish T-bills). All figures are net of fees and ratios in the above charts are calculated using monthly returns. |

May summary

Protean Select returned 0.9% in May, leaving the fund up 3% year to date.

Biggest contributors to returns were Asmodee, Acast (OTCPK:ACASF),and Intea. Detractors include Ambea, Mekonomen, and Truecaller (OTCPK:TRUBF).

Average adjusted net exposure for May was 25%, gross exposure 125%.

Arjo – Low valuation on low expectations

We have built a substantial position in Swedish medtech company Arjo in recent weeks. This is a first for us, as Arjo is a company we have been short on and off for the past few years. We have been critical about strategy, communication, valuation, and capital allocation.

Since demerging from Getinge (OTCPK:GNGBF) in December 2017, the typical “renewed focus” you see from a spin-off has been pointed in the entirely wrong direction. Instead of grinding out efficiency gains and strengthening competitive advantages in the arguably not particularly sexy core business of hospital bed rentals and mobility solutions, the management tried to paint a picture of accelerating growth via launches of “new and innovative products”.

If there is one thing investing in Medtech for the past 20 years has taught us: there is no shortage of innovative products. Acquiring or licensing new shiny things that sound and look great is the easiest thing in the world. Heck, just in Scandinavia, there are 45 listed medical equipment companies with a market cap below 100m EUR, as a testament to the number of hopefuls with a good-enough-story-to-get-funding out there.

The other thing we have learnt is it takes years and years to build a market for new products. Not only do you have to convince a very professional hospital procurement organization of your terrific product, you also need to get the practitioners to actually use it. Which means training, seminars, trade fairs, and a well-versed sales force. In short: it takes a ton of time and effort (and cash).

Regardless of this, the team at Arjo promised the market the product strategy would drive substantial growth “next year”. Analysts (and investors) believed them, adding a couple of percentages to estimates. Only to be disappointed again and again.

The C19-years distorted the market’s perception of Arjo’s earnings power as both margins and revenue expanded for an extended period. The EBIT margins in 2021 were double those in 2018. Unfortunately, like with so many other stocks, the multiple the market was willing to pay turned out to be way too high. Add in the perennial disappointments from new products, and you have a toxic cocktail of falling credibility and negative revision from a too-high valuation starting point.

Contrasting Arjo’s operational stability with the share price and valuation multiple rollercoaster is an interesting exercise.

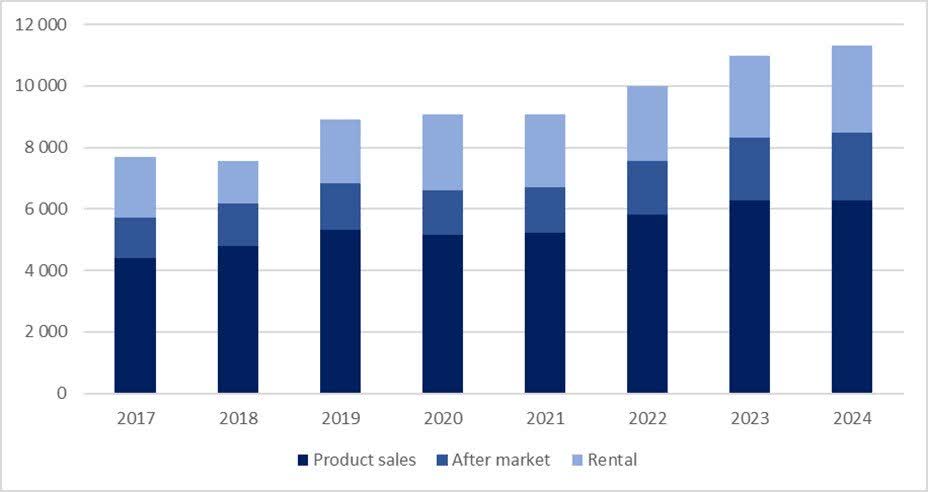

Here is the revenue development on a yearly basis since spin-off:

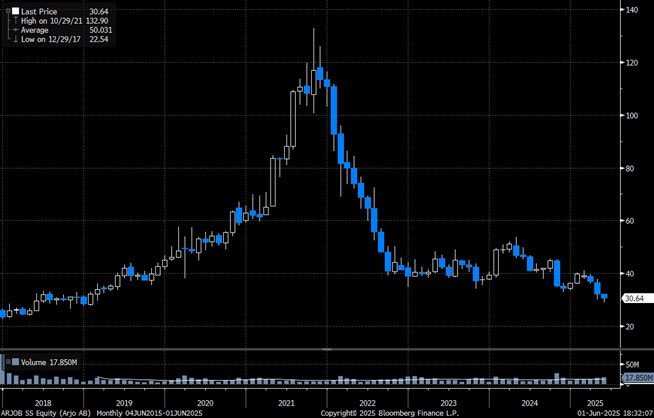

And here is the share price….

ARJO B – Share price development from 2018 – 2025

Then this January, after 8 years and nothing to show for it, the patience of by far the most patient and loyal main owner on the Stockholm Stock Exchange (Carl Bennet) finally wore out. The CEO was sacked unceremoniously, and sent off with a lukewarm thank you for “Arjo has since its spinoff developed into a company with a solid foundation under Joacim’s leadership.” The stock has gone from the 20’s in 2018, to 120 at the peak late 2021, to the 20’s again during May of this year.

This is partly because the past few quarters have been interpreted in a glass-not-even-half-full sentiment: volatile FX movements cause sizeable re-valuations of balance sheet items, tariff uncertainty reduces visibility on margins and competitiveness, a big CEO severance payment, and an organization geared for continued growth that failed to materialize in Q1, causing a miss on OPEX. When everyone who has bought the stock in the past 6,5 years has lost at least 30%, the stock has very few friends, and even fewer that are willing to give them the benefit of the doubt.

It is painful to own a dog like Arjo, where there still are several unhappy holders looking to rid themselves of stock. But low expectations on a low valuation is a powerful starting point. The search for a new CEO is ongoing, and in the meantime, the CFO (whom we rate) is the acting CEO. He makes all the right noises. Back to basics. Stop the nonsense. Improve efficiency. Cut costs. Address structural headwinds asap. We think there are underperforming units that could be divested (like the bed manufacturing in Poland), improving key metrics organic growth and gross margins meaningfully.

Underneath all the hoopla regarding (the now discontinued) newfangled products and their glorious potential, lies a solid business. Organic growth in the past 24 months has averaged 3.9%. The market is in good shape, and there’s nothing wrong with either the core product portfolio or demand. Comps are easy going forward, and there are product upgrades in the core portfolio in the pipeline. This is important. In addition, gross margins are ticking up, and free cash flow is robust. The balance sheet is in good shape, and at the recent AGM, a first-ever 10% buy-back mandate was approved. This is a good signal, considering the main owner has rarely, if ever, used the buy-back tool in any of his many companies.

We think consensus estimates are too low in the short, medium, and long-term. And valuation at these too-low estimates is undemanding. Close to double-digit free cash flow on near single-digit multiples. It appears the main owner and insider Mr. Bennet agrees, as last week he bought 60m SEK worth of stock (approx. 1% of the co). A first trade since building his position just after the spin-off 7 years ago.

If Arjo starts by just meeting expectations, that should be enough for a re-rating. If we are wrong, there is a margin of safety in a modestly valued non-cyclical business with structural options and a solid balance sheet. This is the kind of risk/reward we are happy to take.

Investment companies – Had their day in the sun

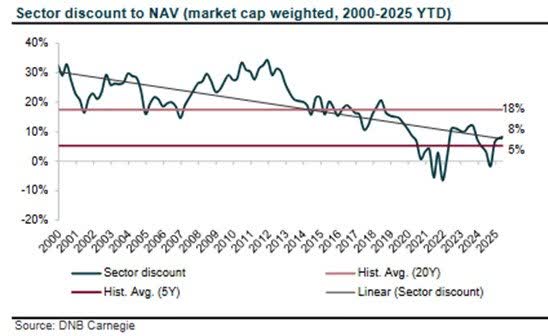

For decades, these odd, listed birds traded at 20-30% discounts to net asset values. Then, in 2012, something happened. Over 10 years, going all the way to 2022, the discounts for the group narrowed, and finally, a premium to NAV between 2020 and 2022. Now they’re starting to trade at a small discount again. What’s going on here?

Two things: interest rates and inflows. The period of tightening discounts correlates nearly 1:1 with the interest rate cycle, which arguably drove valuations of the unlisted portions of the portfolios to previously unseen levels. The emergence of “Investment company mutual funds”, the biggest of which was launched in 2012 (it now manages 5bn USD), created substantial demand for shares. Helped by their success, it is not a foreign thought to think that their buying contributed to the shrinking discounts. The biggest fund of this kind grew so much (i.e. impacted prices so much) that they were forced to widen the scope to include regular listed companies for liquidity reasons. Closing the fund to stay true to the original idea? Oh no, that’s not how fund management works. The financial industry always turns the knob to 11. Or as the saying goes: when the ducks are quacking, feed them.

Fact remains, however, it’s hard not to like investment companies. Have a long investment horizon, avoid silly things, deploy an owner-operator mindset, and keep costs low. It is a winning argument over time. Berkshire Hathaway has won a lot of fans over the years, which means there’s certainly no shortage of hopefuls trying to capitalize on the popularity by launching more and more of them.

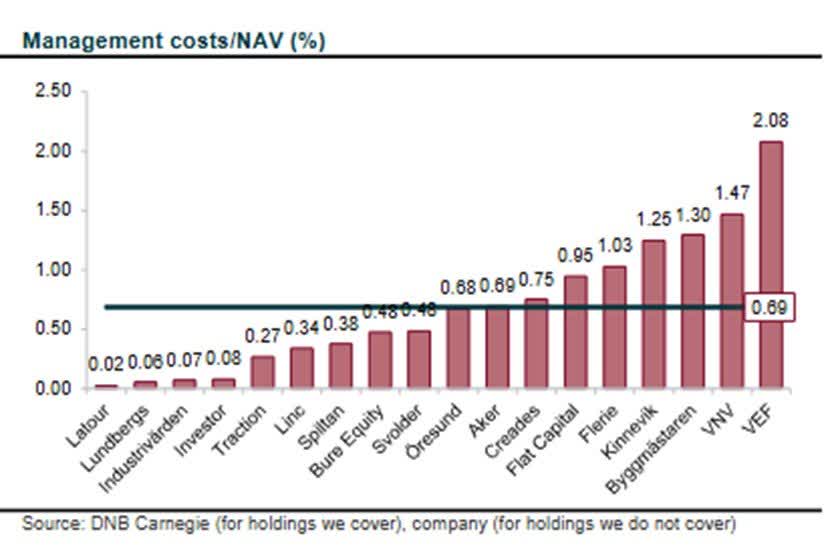

In Sweden alone there are almost 20 listed investment companies. With a long-term horizon and a fixed management cost that does not go up (much) as assets grow, they share the scale advantages with investors. But looking at actual data, you could argue it only works in a very select few (of the sizeable) companies.

The big four have management fees to NAV that are very competitive, but the average for the group is 0.69% (more expensive than our Aktiesparfond!).

Today, almost 600.000 Swedish individuals own shares in Investor AB. That’s great. But we think the interest rate and demand-driven outperformance over the past 10-12 years is ending. Starting points matter. Don’t expect the outperformance to continue.

In fact, it’s already begun to reverse. In the past 12 months, the group has underperformed the broad Swedish SBX index by 6% on aggregate, and the weighted portfolio average P/E is 20x. Not cheap.

Investment companies were a great buy in 2012, at a 30% discount. Today, not so much. We are short a few, as we think they underperform the market from here. Just going back to the 20-year average discount to NAV means 10% additional downside for the sector.

Protean Aktiesparfond Norden – Richard Bråse

Aktiesparfonden is a Nordic long-only fund aiming to generate above-market returns over the long term by active investing in value-creating companies and charging a low fee. A fee that is reduced further as the fund grows, sharing the scale advantages with investors.

Aktiesparfonden, which is daily traded, has per the last day in May returned 6.8% since inception. This is ahead of the benchmark, VINX Nordic Cap, by 4.1% points.

Our communication for Aktiesparfonden is in currently only in Swedish and updates can be found at www.aktiesparfonden.se by clicking the headline “Anslagstavla”.

The fund now manages >500m SEK.

Thank you for your long-term perspective and trust in our process.

Richard

Thank you for being an investor.

Pontus Dackmo | CEO & Investment Manager | Protean Funds Scandinavia AB

The monthly reminderWe optimize for performance, not for convenience, size, or marketing. You can withdraw money only quarterly (monthly in Small Cap). We tell you very little about our holdings. Our strategy is tricky to describe as we aim to be versatile. A hedge fund can lose money even if markets are up. We charge a performance fee if we do well. You do not get a discount if you have a larger sum to invest. We do not have a long track record. Aktiesparfonden’s reminderWe aim to generate above index returns over 3-5 years, but there are no guarantees. The fund is daily traded, but that doesn’t mean you should. To beat the index, you need to deviate from the index. This means taking uncomfortable positions. Be aware that the fund can underperform the index during periods. Sometimes, long periods. We lower the fee as the fund grows. The first 10 basis point cut comes at 10bn SEK in AuM. DISCLAIMER: Investments in a fund can both increase and decrease in value. You are not guaranteed preservation of invested capital. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

2026-05-13")

")

")

")